Welcome to The Weekly!

Not Likely. The US-Israel-Iran war remains far from resolved, and global liquidity will likely continue to ebb for as long as it persists. With the conflict exhibiting few signs of de-escalation, the probability that it devolves into a multi-month overhang for markets increases. Our deep study of economic and geopolitical history leads us to conclude that militaries don’t destroy empires. Egos and excessive debt do.

On the macro side, recent data has been broadly supportive of our GRID Model projections of accelerating growth and slowing core PCE inflation. However, marginally hawkish forward guidance from the Fed, BOJ, BOE, and ECB are signaling that investors who have yet to lower their gross and tighten their net exposures should not expect to be bailed out should the global energy supply shock continue to devolve.

Meanwhile, the January TIC data continues to support our Geopolitically Driven Supply-Demand Imbalance in the Treasury Bond Market thesis, with the widening divergence between foreign demand for Treasury coupons and foreign demand for US corporate stocks and bonds now in plain sight.

As always, members of our global investor community can trust that our institutional-grade risk management overlays—KISS and Dr. Mo—will help our portfolios navigate these emergent risks better than investors attempting to manage risk without systematic rules or relying on fundamental research alone.

In Case You Missed It

Why Is the Next Historic Geopolitical and/or Financial Crisis Likely to Occur Within 5–7 Years?

Enjoy this excerpt from our March 2026 monthly Macro Scouting Report webcast in which we detail some of the math behind our conclusion that the timeline for the US to be mired in a historic geopolitical and/or financial crisis is much, much shorter than the median investor realizes.

Charts of the Week

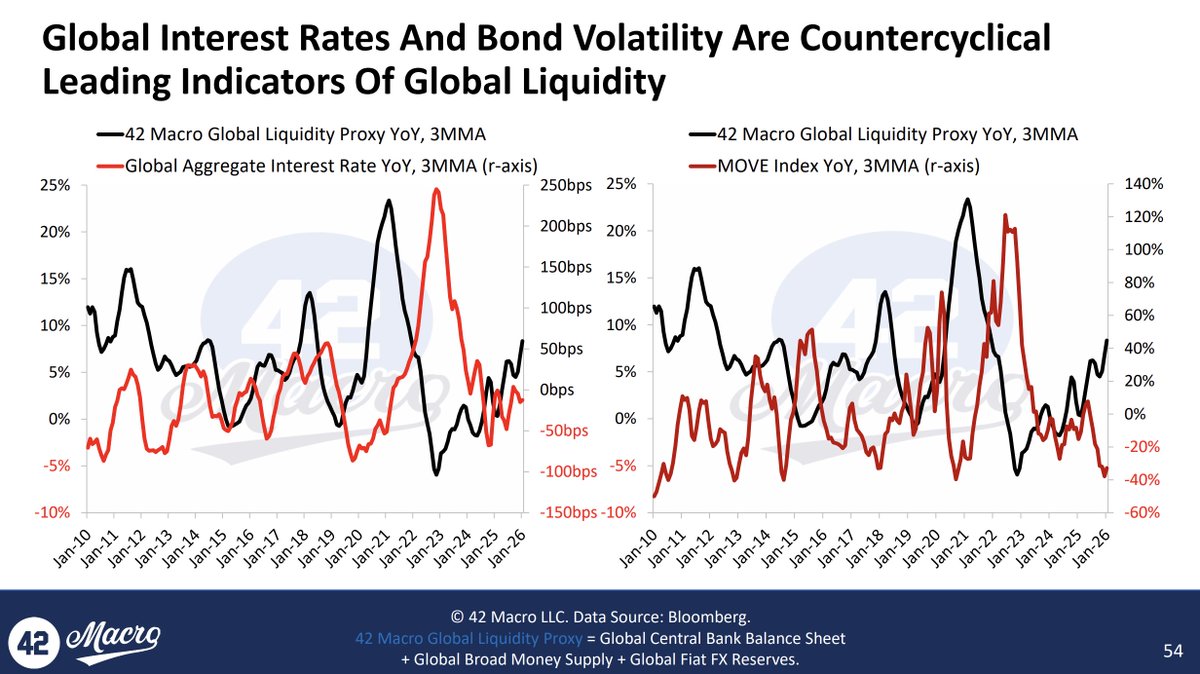

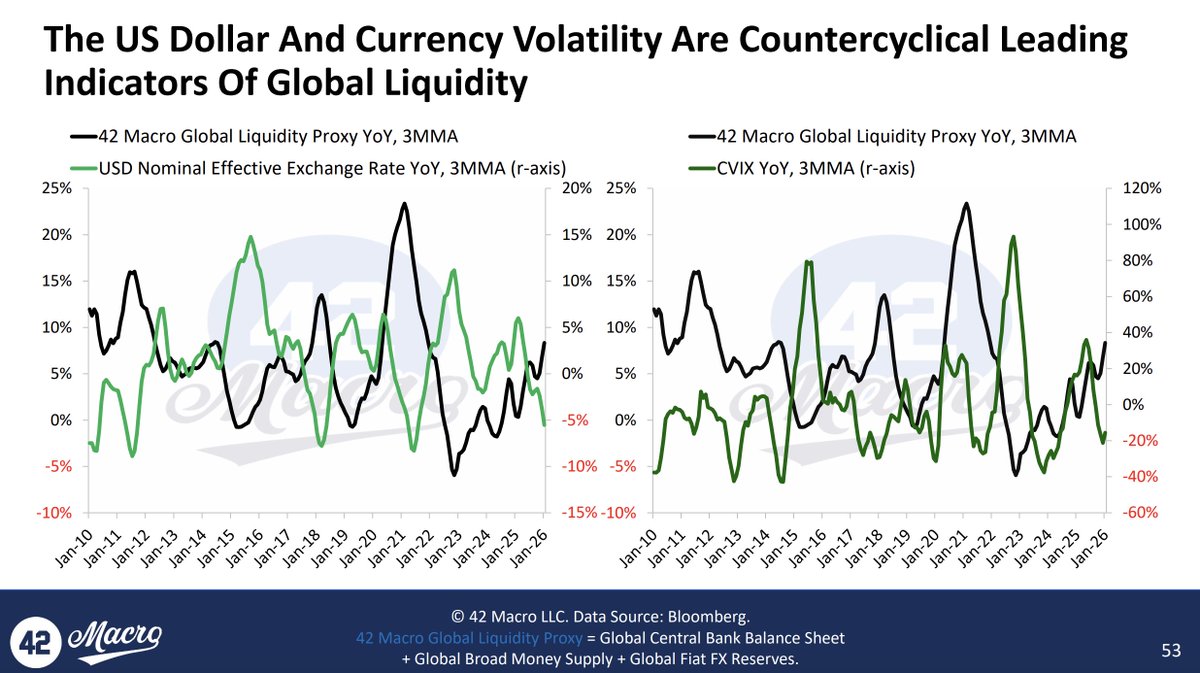

When the dollar, currency volatility, global interest rates, and bond market volatility spikes, global liquidity tends to fall. These countercyclical relationships, tracked here from 2010 to 2026 via the 42 Macro Global Liquidity Proxy, serve as a powerful leading indicator for risk assets.

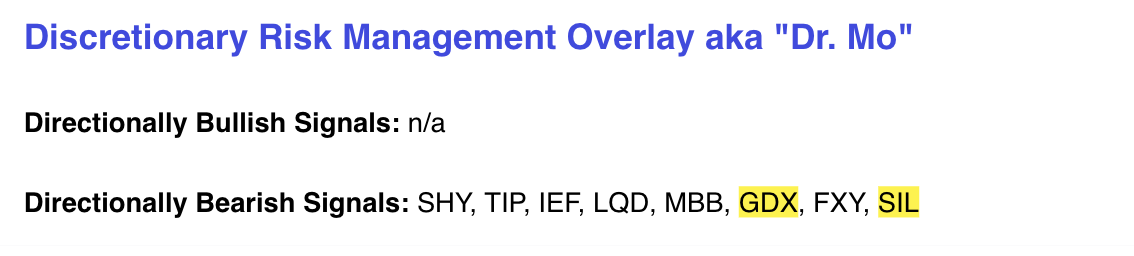

Successful Signals From Dr. Mo

On March 6th, 2026, our Discretionary Risk Management Overlay signaled a bearish breakdown in Gold Miners $GDX and Silver Miners ($SIL). Since the pivot, $GDX and $SIL have crashed -21% and -22%, respectively.

Community Spotlight

This week, we’re excited to share feedback from a member of our global investor community. Specifically, the real-life impact that KISS has had on their mental and physical health.

It’s always rewarding to see KISS and Dr. Mo deliver meaningful outcomes for investors around the world. We truly appreciate your feedback.

EXPLORE 42 MACRO RESEARCH