Welcome to The Weekly!

This week’s defining question was simple but consequential: Did the U.S. administration accidentally and permanently cede control of global energy markets to Iran? Monday’s relief rally, triggered by a Truth Social post announcing a five-day diplomatic pause, gave markets a temporary reprieve, but the underlying dynamics have only grown more complex. Iran began charging vessels for safe passage through the Strait of Hormuz, effectively institutionalizing an informal tolling regime.

Meanwhile, Apollo and Ares imposed draconian withdrawal restrictions on select private credit funds. This is a stark reminder that the geopolitically driven liquidity crisis is already spilling into broader financial markets.

By Thursday, the more pressing question became: Why haven’t stocks crashed yet? The answer lies in Bayesian priors. Most institutional investors entered this conflict with generally positive expectations for five of the six key macro cycles, and there hasn’t been enough time or negative economic releases to catalyze material revisions to GDP and earnings forecasts. Those revisions are forthcoming every week this crisis persists.

As always, members of our global investor community can trust that our institutional-grade risk management overlays—KISS and Dr. Mo—will help our portfolios navigate these emergent risks better than investors attempting to manage risk without systematic rules or relying on fundamental research alone.

In Case You Missed It

A Global Liquidity Crisis Is Underway… What’s Next?

The escalating U.S.-Israel-Iran conflict has moved beyond an energy supply shock and evolved into a global liquidity crisis. In our opinion, investors are underestimating how disruptions in energy flows and capital recycling are tightening financial conditions and reshaping the macro regime.

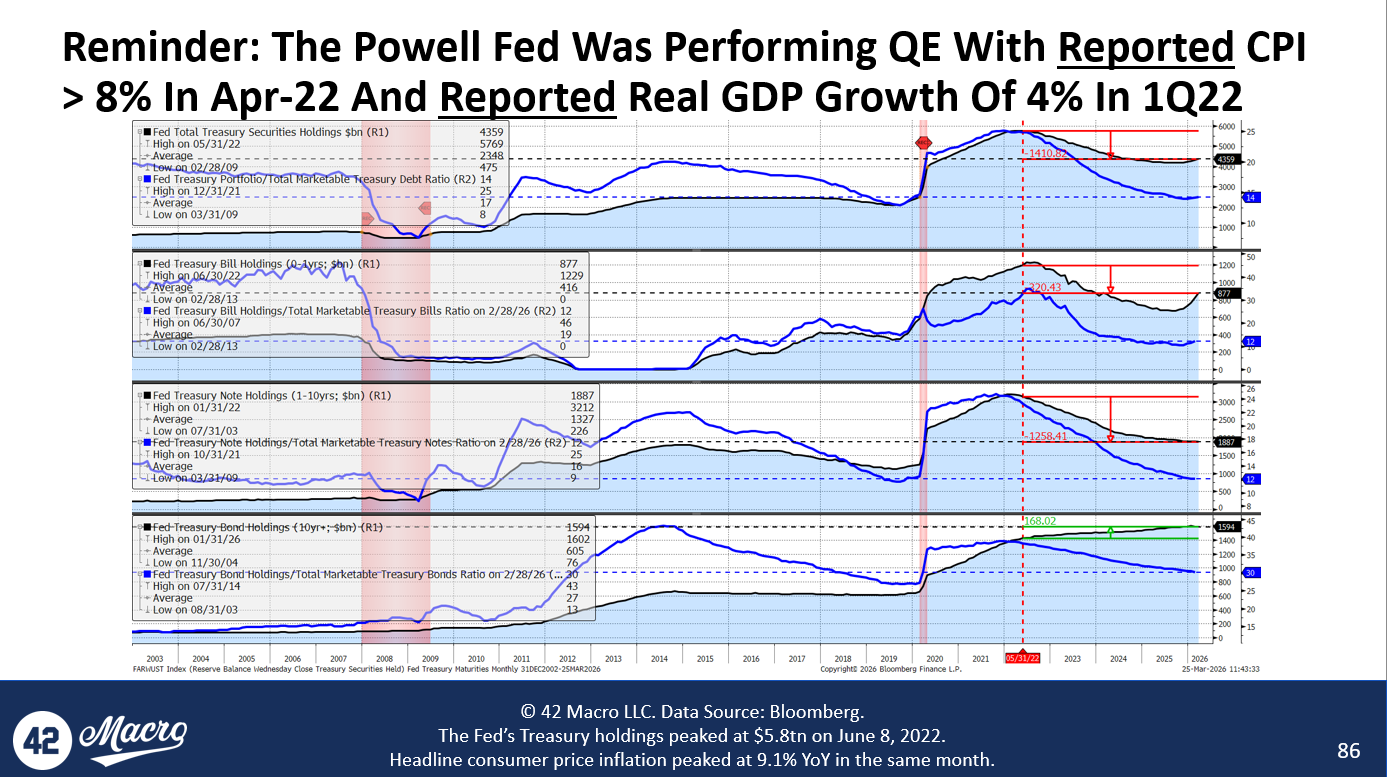

Chart of the Week

The Powell Fed continued expanding its balance sheet deep into 2022, even as inflation exceeded 8% and real GDP growth remained strong. Juxtapose this with the FOMC’s directionally hawkish response to the current negative supply shock and it’s easy to see why members of the political right continue to accuse the Fed of political bias.

As data-driven centrists, we don’t have a dog in this race. We simply wish for better monetary policy outcomes than the legacy of accumulated monetary policy errors from the past ~30 years.

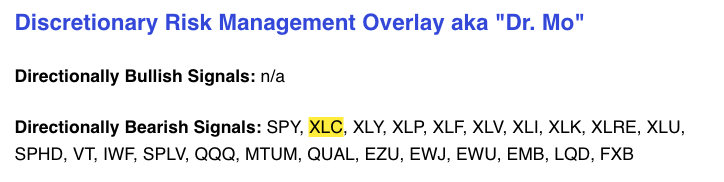

Successful Signals From Dr. Mo

On March 4th, 2026, our Discretionary Risk Management Overlay signaled a bearish breakdown in Communication Services $XLC. Since the pivot, $XLC has corrected 10%.

Community Spotlight

This week, we’re excited to share feedback from a member of our global investor community. Specifically, we are highlighting the personal-best performance investors tend to enjoy once they’ve empowered their investment process with our institutional-grade risk management overlays, KISS & Dr. Mo.

It’s always rewarding to see KISS and Dr. Mo deliver meaningful outcomes for investors around the world. We truly appreciate your feedback.

EXPLORE 42 MACRO RESEARCH