Will Inflation Come Back HOT?

Darius recently sat down with Anthony Pompliano to discuss inflation, its direction, and its effect on asset markets.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. Headline CPI Is Accelerating Again, Primarily Due to Energy

Last month, the 3-month annualized growth rate of headline inflation spiked from just under 2% to 3.9%.

A material increase in energy inflation drove the move.

Until last month, the three-month annualized rate of energy inflation had been negative for approximately one year; the August CPI report indicated an energy inflation increase of 25.4% on a 3-month annualized basis.

We expect the increase in energy inflation to persist as Brent crude oil continues its upward momentum.

2. Core CPI Continues to Decelerate, Primarily Due to Shelter

While Headline CPI is increasing, Core CPI, a measure that excludes some of the most volatile components like food and energy prices and therefore provides a clearer view of the underlying trend in inflation, is decreasing.

Last Wednesday’s report showed that:

- Core CPI decelerated to 2.4% on a 3-month annualized basis – the lowest reading since 2021.

- Core Goods CPI inflected negative to -1.9% on a 3-month annualized basis.

- Shelter Inflation materially impacted Core CPI as it declined from just over 5% to 4.4% on a 3-month annualized basis.

3. Producer Price Inflation Is Back on The Rise Again And May Also Represent The Vanguard of Sticky Inflation

PPI, which measures price changes from the producer’s perspective, accelerated to 4.2% on a 3-month annualized basis – the highest value since the first half of last year.

Leading underlying measures of inflation like Super Core PPI are beginning to show upside momentum and we are starting to see the first signs that inflation is potentially bottoming out.

The return of inflation is negative for asset markets – with it comes a stronger dollar and greater bond market volatility, both of which are headwinds for any increase in global liquidity.

That’s a wrap!

If you found this blog post helpful:

- Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

- RT this thread and follow @42Macro and @42MacroWeather.

- Have a great day!

Buy The Dip Until “Immaculate Disinflation” Transitions To “Sticky Inflation”

A return of inflation pressure destroys the “transitory GOLDILOCKS” narrative and potentially derails the actual GOLDILOCKS US economy that has supported risk assets for the past few quarters, paving the way for a cross-asset crash. Our qualitative research views expect that process to occur within 3-6 months. Our best guess based on the momentum in key inflation time series and the labor market is sometime around yearend or early in the new year.

Emphasis on “guess”. We deliberately never speak in certainties about the future; the only investors that do are those chasing clout on podcasts and social media platforms. Beware conviction from folks that lack the DEEP, DAILY Bayesian inference process required to understand the full distribution of probable economic and financial market outcomes.

If we are wrong on the timing of the handoff from “immaculate disinflation” to “sticky inflation” and it happens much sooner than our 3-6 months [from now] projection, our Global Macro Risk Matrix will transition from risk-on REFLATION to risk-off INFLATION early in that process. Such a shift would be your queue to shift from a buy-the-dip mentality to a sell-the-rip mentality in asset markets. It would also be your queue to pivot defensively from a factor tilt perspective. Until then, we remain constructive on risk in accordance with the “transitory GOLDILOCKS” that we co-authored with our friend Bob Elliott in January.

Evidence Of A Potential Wage-Price Spiral

The ~150,000 member United Auto Workers (UAW) union has declared “war” on Detroit’s big three auto makers GM $GM, Ford $F, and Stellantis $STLAM IM, threatening a strike by September 15 if the companies fail to acquiesce to demands that include a +46% wage increase and a decline in the work week to 32 hours. If a new collective bargaining agreement cannot be achieved by the deadline, the strike will be joined by Unifor — Canada’s largest labor union with ~315,000 total workers and ~18,000 auto workers.

Stories like this are supportive of our view that the narrative around inflation is likely to shift from “immaculate disinflation” to “sticky inflation” within 3-6 months. We have been keen to call out the elevated probability of a soft landing in the US economy. While a soft landing is not our modal outcome, we believe it is a scenario worth educating you on because a soft landing in the economy is highly likely to result in a soft landing in inflation relative to the Fed’s 2% target — which Powell went out of his way to quadruple down on last Friday at Jackson Hole.

No firm on global Wall Street has had a more accurate view on the resiliency of the US economy than @42Macro has for the past year and, as a result, a better call on bonds. We still see more fixed income volatility in the months ahead because we believe the consensus narrative surrounding inflation is likely to deteriorate before the recession hits.

Still No Recession in Sight

From a recession-signaling perspective, we have been watching three statistics that are updated with each month’s Jobs Report: Continuing Claims/Total Labor Force Ratio, Cyclical Unemployment, and Temporary Employment.

- With respect to the Continuing Claims/Total Labor Force Ratio, the 3mo annualized growth rate for July decelerated to -24.6%, well shy of the median rate observed at the start of recessions throughout the history of the time series.

- With respect to Cyclical Unemployment, the 3mo annualized growth rate for July accelerated to -3.3%, well shy of the median rate observed at the start of recessions throughout the history of the time series.

- With respect to the Temporary Employment, the 3mo annualized growth rate for July decelerated to -6.5%, narrowly shy of the median rate observed at the start of recessions throughout the history of the time series and is the only one of our “Fab 5” Recession Signaling Indicators suggesting the US economy is currently in a recession.

With the Fed nearing the end of its rate-hiking scheme, asset markets likely require a recession for the current correction to develop into a crash.

The Most Important Number In Today’s Jobs Report

The spread between Labor Demand (Household Survey Employment + JOLTS) and Labor Supply (Total Labor Force) rose to 3.7mil in July from 3.6mil in June. This statically rare phenomenon of excess labor demand is the key reason wage growth remains robust amid trending “immaculate disinflation” and improving Nonfarm Productivity (3.7% QoQ SAAR in Q2; highest since 3Q20).

The US Economy Is Very Strong

Yesterday, Darius joined Anthony Pompliano to discuss Consumer Spending, Personal Income, Inflation, and more.

In case you missed it, here are the three most important takeaways from the interview:

1. Consumer Spending Has Accelerated In Recent Months

Consumer spending, the total value of all goods and services purchased by households, makes up 68% of GDP.

Last week’s PCE report indicated that Real Personal Consumption Expenditures accelerated to 2.9% in June, primarily driven by a rebound in goods consumption – a three-month high.

In addition, Real Goods PCE accelerated to 5.4% on a three-month annualized basis, also a three-month high.

Both readings suggest US consumers remain incredibly resilient.

2) Accelerating Income Growth Supports Our “Resilient US Economy” Theme

Even if individual real wages are declining, as we have seen recently, overall consumer income can still grow from increased employment, government support, and other income sources.

Nominal Employee Compensation, the broadest nominal measure of income published about the labor market every month, accelerated to 6.2% three-month annualized in June – the highest reading since September last year.

Additionally, Personal Interest Income, the income individuals receive from interest-bearing assets like savings accounts and bonds, accelerated to 8.8% three-month annualized basis in June.

This figure is the highest number we have seen since January of this year and signals that consumers may have more disposable income to spend.

3) The Inflation Fight Is Improving Significantly

Typically, inflation breaks down AFTER a recession. This year, we have seen the opposite – a term referred to as “immaculate disinflation”.

In Friday’s PCE report:

- Core PCE, the Fed’s preferred measure of inflation, decelerated to 3.3% on a three-month annualized basis, the lowest print since February 2021.

- Super Core PCE decelerated to 3.2% on a three-month annualized basis, the lowest print since July 2022.

- Median PCE decelerated to 3.8% on a three-month annualized basis, the lowest print since August 2021.

- Trim Mean PCE decelerated to 3.4% on a three-month annualized basis, the lowest print since August 2021.

We expect the YoY inflation numbers to follow the low three-month annualized rates over the coming months, strengthening the immaculate disinflation narrative supporting asset markets.

That’s a wrap!

If you found this blog post helpful:

- Go to www.42macro.com to unlock actionable, hedge-fund caliber investment insights.

- RT this thread and follow @42Macro and @42MacroWeather.

- Have a great day!

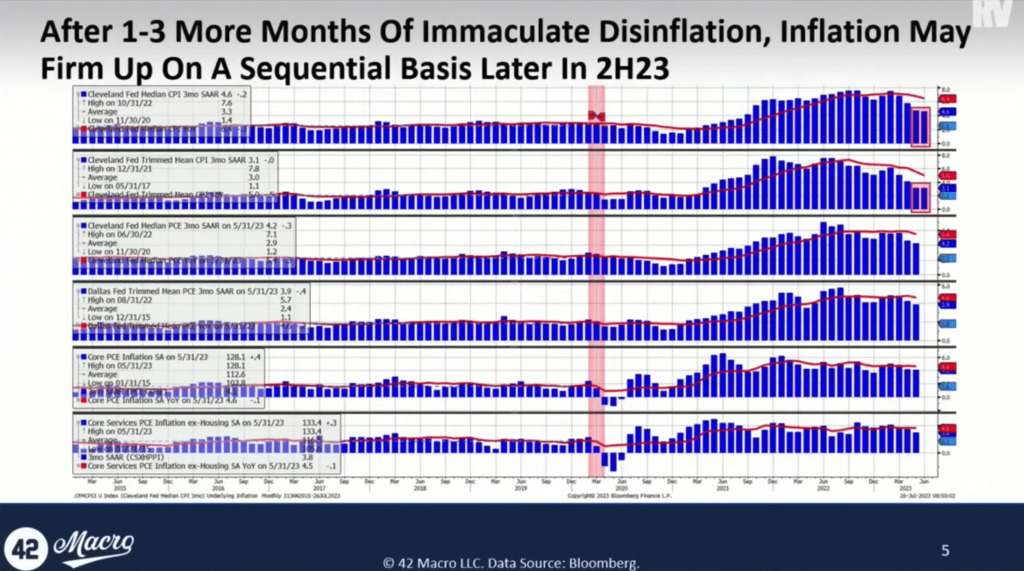

Is the Fed Done Hiking?

Earlier this week, Darius joined Maggie Lake and Andreas Steno on Real Vision to discuss the Fed, Inflation, and more.

If you missed the interview, we have you covered. Here are three key insights that will save your portfolio:

1) We Believe The Narrative Surrounding Inflation Will Change In 3-6 Months

The interplay between immaculate disinflation and rising soft landing expectations has been the driver behind asset markets this year.

We believe any potential shifts in this narrative are not being adequately priced into market forecasts.

Reviewing several key inflation measures—median CPI, trim mean CPI, median PCE deflator, trim mean PCE, core PCE, and super core PCE—highlights a concerning trend. Sequential trends, especially for median CPI and trim mean CPI, indicate stagnation between 3% to 4%. If this lack of progress continues, it could be problematic for the economy.

Our models indicate that a recession in the US economy is unlikely to begin until Q4 this year or Q1 next year, with the depths of the recession probably not hitting until the second or third quarter of next year.

2) The Rate of Change of Inflation Is Important, Not the Level

Investors should be concerned with inflation’s direction and velocity – not the current level.

Why? Because the rate of change is what markets react to. While the Federal Reserve may concern itself with the actual level of inflation, investors should strive to be one step ahead of the Fed, analyzing shifts in the direction and speed of travel.

3) A Soft Landing In Growth = A Soft Landing In Inflation

Inflationary impulses in the economy take time to permeate fully – this explains why the BLS and BEA measure inflation as they do.

Inflation has subsided back to around 2% when you exclude the lagging housing components of inflation.

Notably, core services ex-housing CPI and the core services ex-housing PCE deflator are showing three-month annualized rates of 1.4% and 3.2%, respectively.

If we do have a soft landing, it will likely be at some point in 1H24 — a scenario that, while not the most probable, is far more likely than a near-term recession.

Under these conditions, we believe we would see metrics like super core CPI, super core PCE, and core PCE firm up and begin accelerating again.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/macro-bundle to unlock actionable, hedge-fund caliber investment insights and have a great day!

Is Wall Street Calling The Fed’s Bluff?

Earlier this week, Darius joined Anthony Pompliano to discuss Manufacturing, the U.S. Consumer, Bitcoin, and more.

Miss the discussion? No problem. Here are the three most important insights that can help your portfolio:

1) Healthy Balance Sheets And A Robust Labor Market Are Contributing to a Resilient U.S. Consumer

Since August of 2022, we have consistently maintained the view that the U.S. economy would remain robust, despite recession fears.

June’s retail sales reported a 4.6% increase on a three-month annualized basis and the highest print we have seen in four months – further proof of the resilience of the consumer we have consistently called for.

Additionally, a significant driver of the increase in retail sales, auto sales, accelerated by a striking 23% on a three-month annualized basis.

Two key contributors to this consumer resilience have been healthy consumer balance sheets and a strong labor market.

2) Leading Manufacturing Indicators Point to Near-Term Bottom in the Inventory Cycle

The ISM Manufacturing PMI, the most widely used leading indicator for the broader US manufacturing cycle, recently dropped to 46.0 in June – a new cycle low.

However, the spread between the ISM Manufacturing New Orders PMI and ISM Manufacturing Inventories, which is a leading indicator of the headline index, suggests a bounce in the ISM Manufacturing PMI in the coming months.

A recovery in the inventory cycle would add additional support to the soft landing narrative and incrementally contribute to the epic short squeeze in US equities that we have and continue to call for.

3) S&P 500 and Bitcoin Correlations:

As part of our 42 Macro research, we conduct a multi-factor correlation study, tracking the S&P 500 and Bitcoin in relation to various macro factors.

Recently, the primary driver of the S&P’s performance has been cyclical growth expectations.

Bitcoin, however, is being driven by structural growth expectations, but inversely, and is rallying on potential recession prospects, which would pressure the Fed and other central banks to provide the market with ample liquidity.

Although most investors bundle risk assets into one broader bucket, the reality is that there is often a divergence between what drives different asset markets.

We believe the Fed will begin providing liquidity to the market by the spring of next year, creating a positive environment for risk assets into and through the end of 2024.

That’s a wrap!

If you found this thread helpful, go to www.42macro.com/macro-bundle to unlock actionable, hedge-fund caliber investment insights and have a great day!