Paradigm C And The Resilience Premium

Darius Dale recently joined Anthony Pompliano on The Pomp Podcast to discuss the recent shift towards Paradigm C, the resilience of the U.S. economy, and the evolving roles of stocks, Gold, and Bitcoin within this new policy regime. If you missed the segment, here are three key takeaways that likely have huge implications for your portfolio:

1) Paradigm C Points to a Bull Market

Darius believes the bond market “broke” President Trump on April 9, prompting a shift away from Paradigm B’s economic pain toward Paradigm C—essentially a supercharged return to Wall Street-friendly policies. With trillions in tax cuts and supply-side incentives, this pivot supports the view that stocks may reach new all-time highs by the end of 2025.

Key Takeaway: A shift to Paradigm C increases the likelihood of a strong bull market and record highs by year-end 2025.

2) The Economy Is Stronger Than It Looks

Despite weak headline GDP, underlying data shows strength. Consumers—especially wealthier ones—still have cash to spend, and the services sector continues to drive economic resilience.

Key Takeaway: Don’t be fooled by soft GDP prints—the services sector is powering a resilient economy.

3) Policy Volatility Is the Real Risk

While current trends suggest a favorable outcome under Paradigm C, Darius warns that policymakers may misread market strength as validation, triggering a pivot back to Paradigm B’s aggressive negotiating tactics. Such a shift could destabilize the bond market and reverse recent gains in risk assets. The fragility of global capital account imbalances underscores the risk of heavy-handed tactics.

Key Takeaway: Markets may rally under Paradigm C—but incremental policy missteps could quickly reintroduce downside risk.

Final Thought: Stick To The Process

The market’s optimism hinges not just on policy outcomes, but on the clarity and consistency of those outcomes. As investors price in a shift toward Paradigm C—with its Wall Street-friendly monetary and fiscal largesse—any renewed flirtation with Paradigm B could reintroduce volatility and downside risk. Contextualizing policy signals within the context of our paradigm A-B-C framework and remaining prepared to dispassionately respond to policy pivots will be essential for navigating what comes next.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Capital At A Crossroads

Darius Dale recently joined Julia La Roche for a timely conversation unpacking the Trump administration’s pro-Wall Street-pivot, growing fragility in U.S. capital markets, and how investors should think about positioning in a Fourth Turning world. If you missed the conversation, here are three key takeaways that likely have huge implications for your portfolio:

1) The Trump Put Is Active—But at a Cost

Trump’s softened stance on tariffs and Powell confirms the bond market—not the stock market—forced a pivot. The administration appears to be shifting from Main Street-focused reform—aka “Paradigm B”—to Paradigm C: deregulation, debt-financed tax cuts, and continued fiscal largesse.

Key Takeaway:

Markets are celebrating the pivot, but it suggests a renewed dependence on policy largesse that is largely favorable for Wall Street rather than structural change that is largely favorable for Main Street.

2) Foreign Capital Is Watching Closely

With over 30% of Treasuries held by foreign investors and a $24T net international investment deficit, the U.S. is as vulnerable to capital outflows as any major economy in modern world history. Treasury market dislocations and growing capital outflows resemble emerging-market-style stress. Maintaining investor confidence is becoming more urgent.

Key Takeaway:

The Fed may ultimately need to step in with yield curve control or large-scale asset purchases if foreign demand continues to wane.

3) A New Phase of the Fourth Turning Is Here

Darius notes that generational fatigue with legacy leadership is accelerating, especially in light of perceived policy failures across multiple administrations. The Fourth Turning dynamic is sharpening, with increasing political, economic, and social volatility.

Key Takeaway:

Investors should expect greater uncertainty—but also opportunity—as long-term realignments continue to manifest.

Final Thought: Stay Systematic

Darius sees markets at a critical juncture, where capital outflows, geopolitical fractures, and generational turnover are reshaping macro risk. As he emphasized, understanding the erosion of U.S. fiscal privilege and the deeper forces of the Fourth Turning is foundational. The next repricing won’t just be about growth or inflation—it will reflect how capital responds to a system under stress. Stay vigilant, stay systematic.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

The Paradigm Is Shifting — Are You Positioned for It?

Darius Dale recently joined Felix Jauvin on Forward Guidance to break down why the U.S. economy is undergoing a historic paradigm shift—from Wall Street-led globalization to Main Street-driven reindustrialization. If you missed the interview, here are three key takeaways that likely have huge implications for your portfolio:

1) Tariffs Mark the Beginning of a Multi-Year Economic Regime Shift

Darius explains that the Trump administration’s tariffs are not a short-term negotiating ploy, but the cornerstone of a deliberate shift from a K-shaped, globalized economy (“Paradigm A”) to an E-shaped, reindustrialized economy (“Paradigm B”). This transition, inspired by Fourth Turning dynamics, is designed to compress the gap between capital and labor-even if it means short-term economic pain.

Key Takeaway:

Markets are still mispricing the durability and intent behind these policies. Investors expecting a quick policy reversal or return to the status quo risk being caught on the wrong side of a structural transition that favors domestic labor and reindustrialization over corporate profit margins.

2) A Technical Recession Is Likely—But an Actual Recession Isn’t Guaranteed (Yet)

Despite rising fears, Darius argues that the U.S. is more likely headed for a technical recession (two or more quarters of negative growth) rather than an NBER-defined, broad-based recession—at least for now. Strong private sector balance sheets, labor hoarding, and a healthy base rate for corporate profitability suggest the downturn could be shallow initially.

Key Takeaway:

While risk assets may still fall over the next ~two quarters, the likelihood of a full-blown financial crisis is much lower than in past cycles. But should the transition falter or policy missteps compound, downside risk could still reach -30% to -40% on the S&P 500.

3) Only QE and Fiscal Stimulus Can Smooth This Transition

Darius emphasizes that cutting interest rates alone won’t be enough. The Fed must resume some form of quantitative easing (QE) to offset the current global debt refinancing air pocket, rising yields, and negative fiscal shocks from both tariffs and DOGE spending cuts. The now-House-approved-Senate tax cut plan could help, but execution risk remains given the deficit hawks, high-Medicaid-state-Senators, and “SALTY” Republicans in Congress.

Key Takeaway:

Without QE or meaningful fiscal relief, the economy could suffer prolonged stagnation. Investors must be prepared for a bumpy ride, with significant downside if the Fed and Congress fail to act boldly. Persistent above-target inflation mean the Fed may be too slow to respond.

Final Thought: Positioning for the Paradigm Shift

Markets are still adjusting to the scale and seriousness of the paradigm shift underway. What many dismissed as mere political posturing is now revealing itself as a structural realignment—one that challenges decades of globalization, reshapes corporate profit dynamics, and forces both investors and policymakers to reconsider their playbooks. Whether or not you agree with the direction, the implications are undeniable: positioning for the durability of this transition will be the key differentiator in portfolio performance and resilience.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

The End of American Exceptionalism?

Darius Dale recently joined Víctor Hugo Rodríguez on Negocios Televisión to discuss why markets may not have bottomed yet—and what needs to change before risk assets become attractive again. If you missed the appearance, here are three key takeaways that likely have huge implications for your portfolio.

1) Markets Won’t Bottom Until Three Things Happen

Darius laid out a clear three-point checklist that must be met before investors can confidently reallocate into risk assets:

- The Fed must expand its balance sheet (i.e., QE or liquidity support).

- Consensus earnings and GDP estimates must be revised lower to reflect recession risks.

- Clarity is needed on fiscal policy—specifically, whether Trump’s tax cut package will actually be stimulative and whether the “DOGE” budget cuts will be softened.

Key Takeaway:

We’re still early in all three of these processes, meaning downside risk remains elevated over the next 2-3 quarters. Investors should expect more volatility until policymakers act decisively.

2) Foreign Demand for U.S. Assets Is Cracking

Darius warned that global capital allocators may be stepping back from U.S. Treasuries and equities. As the U.S. turns away from globalization and fiscal prudence, foreign investors are less willing to finance America’s growing deficits. With Congress potentially adding another $5-plus trillion in debt via tax cuts, this shift could put significant upward pressure on long-term yields.

Key Takeaway:

This marks the potential beginning of a structural regime shift in global capital flows—a bearish signal for bonds and a growing risk to U.S. financial stability.

3) The KISS Model Portfolio Is Positioned for Defense

Months ago, Darius moved his own allocation—and that of thousands of 42 Macro clients—into defensive posture. At the time of recording on Tuesday afternoon, the 42 Macro KISS Model Portfolio featured:

- 67.5% Cash

- 0% Stocks

- 30% Gold

- 2.5% Bitcoin

Key Takeaway:

KISS pivoted to 0% equities on March 5th, and will remain in defensive mode until it quantitatively derived volatility targeting and dynamic position sizing signals inflect. The strategy is designed to minimize drawdowns and preserve capital during cyclical bear markets—while also participating in bull markets.

Final Thought: Wait for the Signal, Not the Noise

Markets are still searching for footing in a rapidly shifting macro landscape. As Darius makes clear, this isn’t a moment for hero trades or blind optimism — it’s a moment for discipline. Until we see a dovish policy pivot, meaningful earnings downgrades, and/or clarity on fiscal direction, staying defensive isn’t just smart — it’s necessary. Risk-on will have its time, but we’re not there yet. Let the checklist, not emotions, guide you.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Is Trump Crashing The Market On Purpose?

Is Trump Crashing The Market On Purpose?

Darius Dale, 42 Macro Founder & CEO, joined Anthony Pompliano on The Pomp Podcast to break down the potential market impact of Trump’s economic policies, the Fed’s inflation dilemma, and why the government might be engineering short-term pain for long-term gain. If you missed the podcast, here are three key takeaways that may have huge implications for your portfolio:

1) Is Trump “Kitchen-Sinking” the Economy to Rebuild It?

Darius likens Trump’s approach to President Reagan’s 1980s strategy—short-term pain to reset the system. By implementing tariffs, restricting immigration, and perpetuating maximum uncertainty among investors, consumers, and businesses, the administration appears to be forcing a hard reset toward a supply-side economy. While the long-term goal may be economic expansion, markets are reacting to the immediate downside risks, as uncertainty weighs on growth and sentiment relative to elevated expectations.

Key Takeaway:

While short-term pain may lead to long-term gains, the adverse sequence of policy implementation should not be ignored.

2) Policy Uncertainty Is Freezing Consumer & Business Confidence

Consumer spending has slowed despite rising disposable income, as people increase savings due to economic uncertainty. Businesses are also holding back on investment, with Q4 real business investment contracting over 3%. This hesitation is already showing up in slowing growth data, and if uncertainty lingers, it could push the U.S. into a deeper slowdown than previously expected.

Key Takeaway:

Without clarity on fiscal policy—especially tax cuts and deregulation—the economy and asset markets may struggle to sustain upside momentum.

3) Will the Fed Quietly Raise Its Inflation Target Again?

Darius’ secular inflation model suggests the U.S. equilibrium Core PCE inflation rate has shifted to 2.7-3.3%, making the Fed’s 2.0% target increasingly unrealistic.If growth continues to slow and inflation trends higher in 2025, the Fed will be forced to either tighten policy, risking recession, or revise its target higher to provide more flexibility for market support.

Key Takeaway:

A shift in the Fed’s stance on inflation could be one of the biggest market catalysts of the year, dictating liquidity trends and risk appetite. We expect the FED to cave and provide liquidity, but it may not do so proactively—risking a potential crash.

Final Thought: Navigating an Era of Economic Reset

Markets are in a tug-of-war between short-term economic uncertainty and long-term economic prosperity. A successful shift to a supply-side economy could sustain the economic expansion, but near-term turbulence may be unavoidable. Liquidity trends and Fed policy will determine whether this reset builds strength or triggers deeper downturns. Investors must stay agile and ahead of macro shifts.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Dale: U.S. Growth Slowing Due To Policy Uncertainty

Darius Dale, Founder & CEO of 42 Macro, recently joined Nicole Petallides on Schwab Network to break down market volatility, the resilience of the U.S. economy, and how investors should be thinking about liquidity, policy uncertainty, and positioning. In case you missed the appearance, here are three key takeaways that could shape your portfolio strategy:

1) Liquidity is Likely To Rescue Markets

Despite concerns over short-term volatility, Darius sees a general uptrend in asset markets driven by accelerating liquidity—both globally and within the U.S. As the Treasury General Account (TGA) declines and net debt issuance is restrained, liquidity conditions should remain supportive for risk assets. With the Fed likely ending the Treasury portion of its balance sheet runoff in the next one to two quarters, markets could see even more relief from liquidity tailwinds.

2) Policy Uncertainty Is Slowing Growth, But Not Breaking the Economy

While corporate confidence remains high due to expectations of business-friendly policies, the data shows a real slowdown in U.S. economic growth. Elevated policy uncertainty—at levels seen only during the Global Financial Crisis and the COVID-19 pandemic—is causing businesses and consumers to hesitate on investment decisions. However, Darius does not see this leading to a recession but warns that prolonged uncertainty could trigger renewed hard-landing fears that weigh on markets.

3) Clarity On Bad Policies + Uncertainty Regarding Good Policies = Risk Assets Struggle

Darius revisits his Triple S Framework—Size, Sequence, and Scope—to assess Trump’s potential economic policies, again, emphasizing that sequence is the critical risk factor. If restrictive measures like tariffs and immigration control are implemented first, they could tighten the labor market, drive up wages, and fuel inflationary pressures. Conversely, if pro-growth policies such as tax cuts and deregulation come later, they may help offset these effects. Ultimately, the market’s reaction will depend on the order in which these policies unfold.

Final Thought: Risk On For Now, But Stay Nimble

Despite policy-driven risks, the current market regime remains risk-on, favoring a buy-the-dip strategy in higher beta and cyclical assets. Emerging markets and international equities have outperformed recently, and relative economic trends suggest that outperformance could continue. But with historic policy uncertainty clouding the road ahead, investors should remain adaptable.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape , partner with 42 Macro’s data-driven insights and risk management processes to help you stay on the right side of market risk.

THE MACRO CLASS

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Is The Fed Fighting A Losing Battle Against Inflation?

Darius recently joined Charles Payne on Fox Business to discuss why the Fed’s inflation fight is failing, the limits of traditional economic indicators, and how Trump’s potential policies could impact markets. If you missed the appearance, Here are three key takeaways that could significantly impact your portfolio:

1) The Fed’s 2% Inflation Target is Unattainable

Darius has been warning since January 2022 that the U.S. economy’s equilibrium inflation rate is in the high 2% to low 3% range, making the Fed’s 2% target unrealistic. Despite recent disinflationary trends, inflation remains sticky, and the latest data reinforces the idea that the Fed won’t get back to 2% without causing serious economic damage. Rather than continuing its restrictive policy, the Fed should revise its target higher and adjust accordingly.

2) Traditional Economic Indicators Are Outdated

Darius argues that widely used indicators like the Leading Economic Index (LEI) are outdated and less relevant in today’s economy. Decades ago, manufacturing made up 30% of GDP and 50% of employment—today, it is only 10% of GDP and 14% of jobs. This structural shift means that many recession indicators don’t capture the strength of the modern economy, which remains resilient due to fiscal stimulus and liquidity dynamics.

3) Trump’s Policy Agenda Could Trigger Inflationary or Deflationary Shocks—Depending on Its Sequence

Darius outlines his Triple S framework—Size, Sequence, and Scope—to evaluate Trump’s potential economic policies. The biggest risk? Sequence. If tariffs and immigration restrictions are implemented first, they could disrupt supply chains, tighten the labor market, and push inflation higher before pro-growth policies like tax cuts and deregulation take effect. The market impact depends on how these policies are rolled out and whether the positives outweigh the negatives.

Final Thought:

Liquidity is likely to trend higher through mid-2025, which is supportive for asset markets. That said, policy-driven inflation risks and potential Fed missteps remain key threats. Investors would be remiss to rely exclusively on fundamental predictions amid a historically wide distribution of probable economic and policy outcomes.

If your risk management signals are not keeping you on the right side of market risk, parter with 42 Macro and join the thousands of investors benefiting from our KISS Model Portfolio and our Discretionary Risk Management Overlay, also know as “Dr. Mo”.

THE MACRO CLASS

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

How Will Trumponomics 2.0 Impact Investor Portfolios?

Darius recently joined Charles Payne on Fox Business to discuss the potential impact of President Trump’s economic agenda on asset markets, the importance of observing the market rather than predicting it, and more.

If you missed the interview, here are the three most important takeaways fromthe conversation that have implications for your portfolio:

1) How Will President Trump’s Economic Policies Broadly Impact Markets in 2025?

When assessing the impact of President Trump’s economic agenda, both positive and negative effects on the economy and asset markets are likely.

Specifically, factors such as tariffs, securing the border, and a hawkish shift in Treasury net financing (i.e., less bills + more coupons) are likely to contribute negative supply shocks to the economy and asset markets. Conversely, tax cuts, deregulation, and accelerated energy production could generate positive supply shocks.

Investors should closely monitor the size, sequence, and scope of these policy changes, as they will play a crucial role in shaping asset markets throughout 2025.

2) What is The Likely Impact of Tariffs on Asset Markets?

Although many Wall Street investors cite the Smoot-Hawley example when discussing tariffs, we believe anchoring on that scenario is misguided. The real impact lies in the currency market. China is likely to respond to fresh tariffs by significantly devaluing the yuan, which carries profound implications for global asset markets. Historically, when China devalues the yuan, other major economies follow suit with sympathy devaluations to maintain competitiveness, resulting in a much stronger U.S. dollar.

If a similar pattern emerges in 2025, this would likely lead to a reduction in global liquidity, which is problematic for asset markets in the context of the global refinancing air pocket that may develop later this year.

3) Should Investors Focus On Observing The Market Rather Than Predicting It?

In short, yes. Our number one piece of advice for every investor is: Listen to what the market is telling you. Because asset markets trend far more frequently than they experience changes in trend, it is always best to align your portfolio with what the market is trying to price in, not against it. The trend is your friend.

Whether we are in an inflationary or deflationary environment, the most consistently successful strategy across all market conditions is trend following.

To successfully remain on the right side of market risk, investors must rely on signals from proven risk management systems (e.g., KISS and Dr. Mo) far more than their gut feel, emotions, or understanding of company or economy fundamentals.

Since our bullish pivot in January 2023, the QQQs have surged 81% and Bitcoin is up +328%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just macro insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.

Best of luck out there,

— Team 42

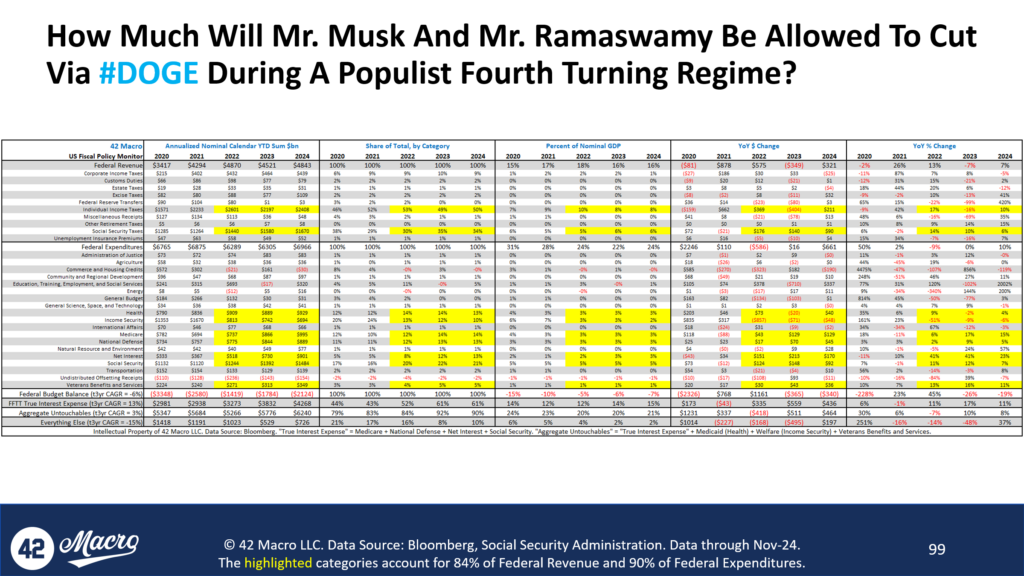

What Must Be Done To Prevent DOGE From Failing?

Darius recently sat down with FFTT Founder and President Luke Gromen to discuss how marketable U.S. treasury market dynamics have shifted over recent years, the likelihood of a meaningful reduction in the federal budget deficit in this Fourth Turning, and more.

If you missed the interview, here are the two most important takeaways from the conversation that have significant implications for your portfolio:

1. How Have Changes In Ownership Structure Contributed To Price And Yield Dynamics In The Treasury Market?

At 42 Macro, one of the ways we analyze the marketable U.S. Treasury market is by segmenting it into various investor cohorts:

- The Federal Reserve: The Fed’s share has been declining due to balance sheet runoff, peaking at 25% in late 2021 and now at only 15% of total marketable Treasury securities.

- Commercial Banks: Banks’ market share decreased from early 2022 until late 2023, when it began to stabilize. This stabilization was driven by programs like the Bank Term Funding Program (BTFP) and expectations that the Federal Reserve would dramatically lower interest rates. Currently, their share is around 15%, well south of the peak of 33% in 2003.

- Foreign Central Banks: The decline in global trade and the steady shift away from global dollar recycling led by the BRICS member nations caused foreign central banks’ share to steadily decline to 14% from a peak of 40% during the 2008 global financial crisis.

- Global Private Non-Bank Sector (Investors): This cohort has become the largest holder of marketable U.S. Treasury securities, with its share increasing from 36% in late 2021 to 55% today.

This shift in ownership has structurally altered the Treasury market. Unlike banks—such as the Fed, foreign central banks, and commercial banks which purchase Treasurys to satisfy policy or regulatory mandates (e.g., Dodd Frank, Basel III and IV)—global investors demand ex ante returns to compensate for taking risk in their portfolios.

As a result of this seismic shift, upward pressure on yields has intensified, signaling a more acute phase in the evolution of Treasury market dynamics and expectations.

2. How Likely Is Significant Reduction In The Federal Budget Deficit During This Fourth Turning?

Our analysis of U.S. federal budget dynamics highlights significant challenges to achieving meaningful deficit reduction.

First, U.S. federal expenditures currently represent roughly a quarter of U.S. GDP—the highest share since at least 1970 excluding COVID and the GFC. Thus, significant cuts would likely catalyze a downturn in the economy—however beneficial a smaller government would be in the long run, which is something both Darius and Luke agree with. Per Luke, the last three recessions saw the U.S. federal budget deficit widen by 600bps, 800bps, and 1,200bps.

Secondly, our research indicates that approximately 90% of the budget is effectively untouchable. This “Aggregated Untouchables” category includes “True Interest Expense”—comprising Medicare, National Defense, Net Interest, and Social Security—along with Medicaid, Welfare, and Veterans’ Benefits. Collectively, these expenditures represent programs unlikely to face cuts under the current pro-populist political climate and are compounding at a rate of +3% per year (+13% per year in the “True Interest Expense” category). The remaining 10% of the budget, which largely includes discretionary spending, amounts to just over $700 billion and has already been shrinking at a compound rate of -15% per year over the past three years.

Lastly, demographic trends are exacerbating the fiscal burden. By 2025, 160,000 people will join the retirement-age population each month, compared to just 32,000 entering the working-age population.

Given these dynamics, meaningful deficit reduction appears improbable without tackling politically protected categories. This leads us to believe that meaningful austerity is an unlikely path forward in the context of this current Fourth Turning environment—especially without a significant devaluation of the US dollar preceding it.

Since our bullish pivot in November 2023, the QQQs have surged 42% and Bitcoin is up +190%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just high-quality insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.

Is The Fed On The Precipice Of Another Major Policy Mistake?

Darius recently hosted Unlimited Funds CEO Bob Elliot on this month’s 42 Macro Pro to Pro, where they unpacked the Fed’s asymmetrically dovish reaction function, the impact of the work-from-home phenomenon, their systematic approaches to investing, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. What Is Driving the Fed’s Expansionary Monetary Policy?

We authored our “Resilient U.S. Economy” theme in September 2022, and since then, we have identified a new contributing pillar: the continuation of expansionary monetary policy.

We believe this policy direction is puzzling, driven largely by the Fed’s belief that no further cooling in the labor market is needed to achieve 2% inflation—a stance we view as highly likely to be inaccurate. Nevertheless, it remains the Fed’s current perspective.

Bob Elliot offered an insightful take on this issue, suggesting that the Fed’s position likely stems from a fundamental disconnect between how academics interpret markets and models versus how practitioners do. This divergence may explain their controversial outlook on the labor market’s role in achieving their desired inflation target.

2. How Is The Work-From-Home Phenomenon Affecting Labor Market Dynamics?

At 42 Macro, we monitor various workforce dynamics metrics, including Nonfarm Productivity Growth and the Private Sector Quits Rate. Our analysis shows that Productivity Growth is currently above trend, while the Private-Sector Quits Rate has declined significantly from its elevated levels over the past couple of years.

We believe this shift toward longer employee tenures is likely a key driver behind the current above-trend rate of productivity growth, as longer retention generally leads to greater employee efficiency. This increased productivity is helping to offset some of the inflationary pressures stemming from higher wages and income growth, and we believe it is likely to persist.

Additionally, the rise of remote work plays a significant role in this dynamic. With the flexibility to live and work from virtually anywhere, employees are more likely to stay with their current employers, further contributing to lower turnover and increased productivity.

3. Why Did We Replace Core Fixed-Income Exposure with Gold in Our KISS Portfolio?

One of the recent adjustments we made in our systematic KISS Model Portfolio was to replace our core fixed-income exposure with gold. This decision reflects our understanding that if our Investing During A Fourth Turning Regime analysis proves true over the long term, it is highly unlikely that bonds will outperform other assets on a real, risk-adjusted basis.

While we recognize that no one—including us—is ever 100% correct on their fundamental views, even partial accuracy in our predictions suggests a strong likelihood that assets like gold, Bitcoin, stocks, and real estate will prove to be far better hedges against accelerated monetary debasement and financial repression than bonds. Indeed, we expect monetary debasement and financial repression to be tools that the Fed employs to address the challenges of excessive sovereign debt and a robust economy that leaves little incentive for buyers of government bonds.

Given this dynamic, we pivoted entirely out of core fixed-income exposure and allocated that portion of our systematic KISS Model Portfolio to gold in October. Our 60/30/10 trend-following strategy now features maximum allocations of 60% stocks, 30% gold, and 10% Bitcoin.

Since our bullish pivot in November 2023, the QQQs have surged 37%. Momentum $MTUM is up +48% and Bitcoin is up +169%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it’s time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just macro insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.