Is There Further Upside Risk In Asset Markets?

Darius joined David Hunter last week on our Pro to Pro Live to discuss the 42 Macro Positioning Model, the outlook for asset markets, our “Green Shoots Globally” theme, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. Our Positioning Model Suggests There Is Likely Additional Risk To The Upside Over The Medium Term

Bears have found themselves reluctant to join the recent rally in equities.

Our 42 Macro Positioning Model monitors the aggregated non-commercial net length as a percentage of total open interest in the combined futures and options markets for US Equities. Currently, this indicator sits in the 33rd percentile of readings, notably lower than the median reading of the 62nd percentile seen at major bull market peaks.

Despite the significant market rally, we have yet to witness the structural upside capitulation characteristic of bull market peaks. This absence suggests there is likely potential for further upside over the medium term, although there may be a correction in the near term.

2. Cash On The Sidelines Stays On The Sidelines Until There Are Reasons For It To Exit

Currently, over $6 trillion is parked in money market funds.

Our analysis, spanning the last four cycles—2020, 2008, 2001, and 1991 —reveals a consistent pattern: cash on the sidelines tends to stay put in these funds until after a crash, recession, and rate cuts have each taken place.

We anticipate this cycle will follow suit, with the bulk of cash on the sidelines staying put until these pivotal events unfold.

3. “Green Shoots Globally” Continues To Support Risk Assets

In January, we authored our “Green Shoots Globally” theme that was supportive of asset markets.

The theme persists, as our models show that every major economy in the world has a Composite PMI trending higher—a bullish leading indicator suggesting what is likely to occur over the next three to six months from an economic standpoint.

Moreover, we track the number of industries reporting growth in the ISM Manufacturing survey. In December, that number bottomed. Our backtests have found that in the year following the bottom, the S&P generates a median return of 28%. While this is just one data cyclical framework to respect, it strongly suggests that the broadening of market breadth stemming from improving global fundamentals is likely to continue.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

Managing Risk in a Risk-On Environment

Darius joined Caroline Woods on Schwab Network last week to discuss the current risk-on Market Regime and its implications for asset markets.

If you missed the interview, here is the most important takeaway from the conversation that has significant implications for your portfolio:

The Market Remains In A Risk-On Regime, And We Believe It Has Room to Run

- At the beginning of the month, our Positioning Model flagged an elevated risk of a short-term correction. While some investors point to geopolitical factors as the cause of the correction, we believe the market was stretched thin in terms of positioning and needed a cooling-off period.

- We believe the market rally will continue because several fundamental themes, including our “Resilient US Economy,” “China Front Loading Stimulus,” “Green Shoots Globally,” and “Jay and Janet Want A Soft Landing,” may contribute to upside risk in asset markets. Until the drivers causing these themes dissipate, we expect asset markets to perform well.

- Although the Fed is discussing rate cuts this year, we maintain that the resilience of the US economy negates the need for cuts, as the economy continues to grow at an at-or-above-trend pace on a real basis and at a well-above-trend pace on a nominal basis. The hawkish repricing of policy rate expectations is bearish, but only to a point in this context. Said simply, the resilient US economy is unlikely to require rate cuts anytime soon.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

What Does REFLATION Mean For Your Portfolio?

Darius joined Adam Taggart on Thoughtful Money this week to discuss the current REFLATION Market Regime, the resiliency of the US economy, the US consumer, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. Investors Should Position In Line With The Current REFLATION Regime

Our 42 Macro Risk Management Process simplifies complex market dynamics into a straightforward three-step approach:

- Position for the Market Regime

- Prepare for regime change using quantitative signals with our Macro Weather Model

- Prepare for regime change using qualitative signals via our fundamental research

Currently, we are in a REFLATION Market Regime. In this environment, investors should consider the following key portfolio construction considerations:

- Risk Assets > Defensive Assets

- High Beta > Low Beta

- Cyclicals > Defensives

- Growth > Value

- Small & Mid Caps > Large Caps

- International > US

- EM > DM

- Spread Products > Treasurys

- Short Rates > Belly > Long Rates

- High Yield > Investment Grade

- Industrial Commodities > Energy Commodities > Agricultural Commodities

- FX > Gold > USD

To consistently stay on the right side of market risk, investors should position in accordance with the prevailing Market Regime.

2. The Resilient US Economy Does Not Require Rate Cuts, But The Fed Wants To Cut Rates Anyway

According to the March 2024 Fed Dot Plot, the Fed is guiding to three rate cuts in 2024, three in 2025, and three in 2026.

At the same time, the US Economy continues to prove resilient across various metrics, including income, consumption, and the labor market.

While we maintain the view that the resilience of the US economy does not justify rate cuts, the Fed’s inclination towards cutting rates has served as a positive driver for asset markets.

3. The US Consumer is Resilient Because of The West Village-Montauk Effect

The essence of the “West Village-Montauk Effect” can be summarized as follows: With a substantial stock of savings, there is less pressure to save a significant portion of your disposable income.

We are witnessing this effect in relation to the US consumer. Since the close of 2019, both households and corporations have experienced a boost in wealth:

- Household cash reserves have surged by 135%.

- Corporate cash reserves have increased by 51%.

- Household and corporate net worth have soared by approximately 34%, outpacing inflation.

This notable growth primarily occurred due to government spending during 2020 and 2021, which included COVID-related tax breaks, forgivable PPP loans, and extensions of jobless claims. A considerable portion of this expenditure entered private sector balance sheets. Simultaneously, as household and corporate net worth expanded, the monthly flow of US Personal Savings turned negative, demonstrating the eagerness of US consumers to spend a higher share of their disposable income due to the elevated stock of savings.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

What Does “Sticky Inflation” Mean For Your Portfolio?

Darius joined Anthony Pompliano this week to discuss inflation, the “No landing” vs. “Soft landing” debate, the Fed, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. The “No Landing” Scenario Is The Highest Probability Outcome Over The Next 12 Months.

The “Soft landing” vs. “Hard landing” vs. “No landing” debate continues. We define a “Soft landing” as a period of trend or below-trend GDP growth, facilitating a gradual return of inflation to trend over time. Conversely, a “Hard landing” signifies a period of GDP growth significantly below trend, which triggers a contraction in the labor market and ultimately leads to a recession. In contrast, a “No landing” scenario entails GDP growth at or above trend, enabling inflation to decelerate but not return to its 2% target.

Our analysis indicates that a “No landing” scenario is the most probable outcome over the next 12 months.

We employ two distinct models to forecast inflation. While the median forecast from these models suggests incremental disinflation in the upcoming quarters, by the fourth quarter, we anticipate bottoming at a level higher than the Fed’s 2% target. This scenario is likely to inflict pain on asset markets once policymakers react to this new reality.

2. Regarding Inflation, 3% Is Likely To Become The New 2%

In our recent deep dive into our secular inflation model, we found a noteworthy key takeaway: we anticipate that 3% will become the new inflation benchmark, replacing the previous benchmark of 2%.

We believe the Fed will acquiesce to 3% being the new 2%. This shift in perspective seems to be gaining traction, as evidenced by Chair Powell stressing inflation would return to its target “over time” during the March FOMC meeting.

While this transition will not unfold in a linear manner, we foresee that over the next few years, the Fed will embrace 3% inflation as the preferred target over 2% if getting inflation sustainably down to 2% will require a recession. This likely policy regime shift is structurally bullish for risk assets and structurally bearish for Treasury bonds.

3. A Variety Of Factors Have Contributed To The Recent Uptick In Inflation

We analyze several key metrics from the Cleveland Fed: the Median CPI, Trimmed Mean CPI, Median PCE Deflator, and Median Trimmed Mean PCE Deflator. Here is a breakdown of the latest figures:

- The Median CPI stands at 5% on a 3-month annualized basis, approximately double its pre-COVID trend.

- The Trimmed Mean CPI stands at 4.4% on a 3-month annualized basis, more than double its pre-COVID trend.

- The Median PCE Deflator sits at 4.1% on a 3-month annualized basis, approximately double its pre-COVID trend.

- The Trimmed Mean PCE Deflator, also on a 3-month annualized basis, stands at 3.7%, more than double its pre-COVID trend.

The surge in these inflation metrics is suggestive of a broad-based acceleration and a preview of what we are likely to witness towards the end of the year as inflation struggles to bottom at a level consistent with the Fed’s 2% target.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

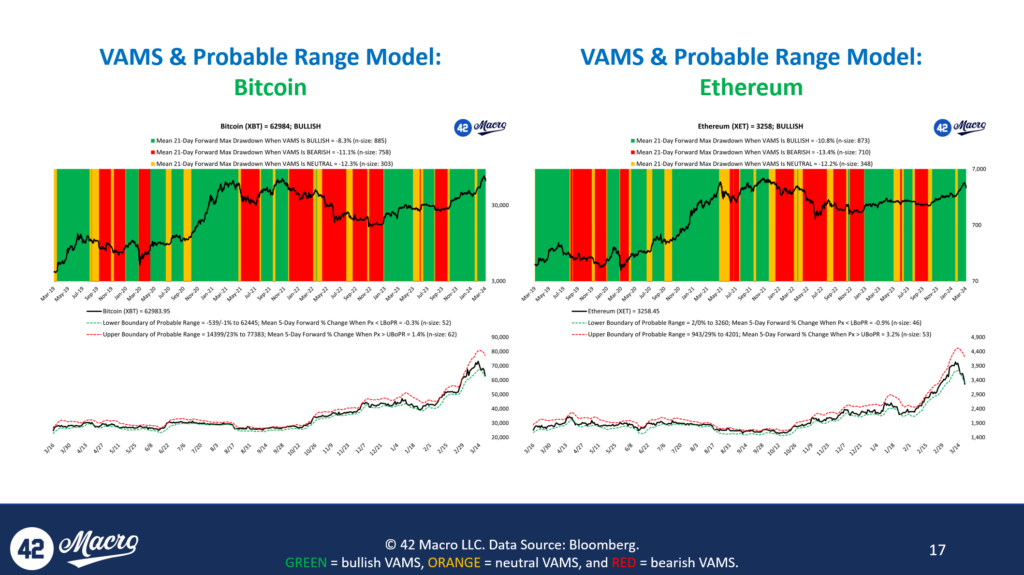

A Glimpse Into Bitcoin

Darius joined Dylan LeClair last week to discuss the outlook for Bitcoin, how it fits into the 42 Macro KISS Model Portfolio, ETF flows, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. Understanding The Correlation Between Bitcoin’s Price And Volatility Is Crucial to Grasping The Dynamics of The Asset Class

Our research at 42 Macro indicates that although equities and fixed income are generally inversely correlated to volatility, Bitcoin tends to be positively correlated to its historical and implied volatility.

Moreover, our 42 Macro Volatility Adjusted Momentum Signal (VAMS) scores volatility relative to price to determine whether an asset is bullish, bearish, or neutral.

Following our VAMS signals has allowed our clients to be on the right side of market risk and remain long during Bitcoin’s large upswings this year. Investors who plan to add Bitcoin to their traditional multi-asset portfolio would be well advised to understand the correlation between Bitcoin’s price and volatility to ensure they are positioned for its large, volatile moves. At 42 Macro, we can help you do exactly that.

2. Investors Can Prudently Gain Exposure to Bitcoin Through The KISS Model Portfolio

Our KISS Model Portfolio, a 60/30/10 trend-following approach, helps clients gain exposure to Bitcoin from legacy strategies such as the traditional 60/40 portfolio.

The current allocation of our KISS Model Portfolio, determined using our Global Macro Risk Matrix and VAMS for dynamic position sizing, is 10% in Bitcoin, 60% in SPY, 15% in AGG, and 15% in USFR.

Although we have a positive outlook on Bitcoin’s future performance, mere belief is not sufficient to allow us to take a position. Our decision-making process relies on signals derived from the current market regime and signals from our VAMS. At 42 Macro, we help investors make money and protect gains in financial markets, and it is through strategies like KISS that we have empowered our clients to achieve these objectives.

3. The 2024 Bitcoin ETF Inflows Have Far Exceeded Expectations

The immediate success of the Bitcoin ETF out of the gate has been remarkable.

IBIT has been the most successful ETF launch in history, gaining an impressive $15 billion in AUM in the first two months.

However, Dylan informed our audience that the current demand for Bitcoin has primarily originated from Blackrock, Fidelity, and other institutional investors. Additionally, ETF issuers have indicated that the current buyers of BTC ETFs do not represent some of the largest pools of capital; those significant investors have yet to enter the market. As a result, we anticipate a fresh surge of capital inflows into the asset class in the coming quarters, which is poised to drive prices even higher.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

Bitcoin, Stocks All-Time Highs: Remain Bullish?

Darius joined Anthony Pompliano last week to discuss the outlook for inflation, global liquidity, asset markets, and more.

If you missed the interview, here are the three most important takeaways from the conversation that has significant implications for your portfolio:

1. The February CPI Report Showed Signs of Sticky Inflation

The February CPI report did incremental damage to the immaculate disinflation narrative.

Headline CPI accelerated to 3.9% on a three-month annualized basis, more than double its pre-covid trend. The spike was largely driven by an acceleration in Energy CPI to 4.5% on a three-month annualized basis.

Moreover, Core CPI accelerated to 4.1% on a three-month annualized basis. The increase was largely driven by Services CPI, which remained at 6.0% on a three-month annualized basis, and Super Core CPI, which accelerated to 6.7% on a three-month annualized basis, more than triple its pre-Covid trend.

2. The February NFIB Small Business Optimism Survey Supported The Soft Landing Scenario

The February NFIB Small Business Optimism survey, a monthly survey that provides insights into the confidence levels and outlook of small business owners, indicates that inflation may continue declining over the medium term.

The sub-indices of the survey, including the Higher Prices, Price Plans Next Three Months, Compensation, and Compensation Plans indices, all slowed sequentially and are at multi-year lows.

These readings suggest that although we see signs of sticky inflation in the CPI and PCE Deflator reports, stickiness is likely to be transitory and that inflation will resume its downtrend over the medium term.

3. Global Liquidity Is Likely to Continue Trending Higher Over The Next One to Two Quarters

The monetary policies implemented by the PBOC this year have been very positive for global liquidity. Additionally, China recently revealed ambitious economic targets for 2024, aiming for a 5% GDP growth, the creation of over 12 million jobs, and a 3% inflation rate. To meet these aggressive economic targets, the PBOC will likely continue easing policy, and that is likely to continue supporting global liquidity.

Moreover, several key countercyclical drivers of global liquidity have supported liquidity creation in the private sector.

The dollar, bond market volatility, and currency market volatility have all trended in directions that support private sector liquidity creation, and we believe these trends are likely to continue over the next quarter or two.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

Is Bitcoin Going to $250k?

Darius sat down with Anthony Pompliano last week to discuss the outlook for Bitcoin, global liquidity, reducing portfolio risk, and more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. Our Models Indicate Bitcoin Is Likely to Remain Bullish Until At Least Mid-Year

The 42 Macro Weather Model is currently generating a bullish outlook for Stocks, Bonds, and Bitcoin over the next three months. These bullish signals suggest each asset class is likely to experience above-median returns over the next three months relative to baseline.

Given these favorable conditions, now is an excellent time to take risks in the markets – a stance we have advocated to our audience since November.

2. China Has Been A Dominant Driver of Global Liquidity This Year

In mid-December, we authored a view that China would front-load policy support at the beginning of this year.

That is what we have witnessed, as the PBOC has been actively implementing monetary policies to support the economy. Its balance sheet is expanding, claims on banks are rising, and it is reducing various policy rates while committing to providing additional lending to specific sectors of the economy.

However, we believe the positive global liquidity impulse is likely to dissipate in the second half of the year. To stay on the right side of market risk, investors must identify these shifts in global liquidity in real time and position their portfolios accordingly. Our Macro Weather Model and Global Macro Risk Matrix are among the best available tools for that.

3. Bitcoin Is Best Managed In The Context of A Traditional Multi-Asset Portfolio With Risk Management Overlays

Bitcoin ETFs have seen record-breaking volumes since their launch in January. As of the market close on February 28th, ETFs reached a volume of $7.6 billion, surpassing previous records.

However, investors in ETFs lack the risk management overlays offered by our 42 Macro KISS Model Portfolio. As a result, many may find themselves max-long Bitcoin during significant drawdowns. Bitcoin has experienced four drawdowns of -75% or more and another two in excess of -50%. That is six times investors could have lost half-to-four-fifths of their money in the asset class.

In contrast, our KISS portfolio, a 60/30/10 trend-following portfolio comprising SPY, AGG, and FBTC, has delivered an average annual return of +13% since 2018, with a maximum drawdown of -11%. Without our risk management overlays, investors would have seen similar returns in a 60/30/10 SPY/AGG/Bitcoin portfolio with a maximum drawdown of -26% and three crashes in excess of -20% since the start of 2019.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

Will The US Economy Enter A Recession?

Darius sat down with Chris Berg recently to discuss the outlook for asset markets, the probability of a recession, the Fourth Turning, and more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. The US Economy Is Likely to Avoid A Recession In 2024 If Productivity Growth Remains Above Trend

Productivity, as measured by output per hour in the US labor market, is showing robust growth at 2.7% year-over-year, surpassing the 10-year, 30-year, and 50-year averages of approximately 1.7%.

To achieve a soft landing, at least two of the following three conditions are typically required:

- Sustained at-trend or above-trend productivity growth

- Rate cuts

- At-trend or above-trend fiscal spending

Presently, productivity is above-trend, money markets have effectively already priced in rate cuts, and we are likely to see above-trend fiscal spending in the current election year.

In the event of a recession, our analysis suggests that it is unlikely to materialize until 2025 at the earliest.

2. We Believe The No-Landing Scenario Is Likely to Become The Modal Outcome Over The Next One to Two Quarters

While a soft landing signifies achieving at or below-trend growth, facilitating the return of inflation to the Fed’s 2% target, a no-landing scenario entails sustaining growth at or above trend levels, preventing disinflation from bottoming at 2%. Conversely, a hard landing is a scenario where the economy enters into a recession.

In the past four months, there has been a notable decrease in the likelihood of a hard landing. Meanwhile, the probability of a no-landing scenario is on the rise, although a soft landing remains the modal outcome for now.

However, we anticipate that the no-landing scenario is likely to become the modal outcome over the next one to two quarters. This expectation stems from our belief that nominal real economic growth is poised to surprise to the upside through the first half of this year across major economies worldwide.

3. The Fourth Turning Will Have Significant Implications For Investors’ Portfolios

Last fall, our team performed an empirical deep dive on the Fourth Turning, a theory sparked by Niel Howe, mentor and former colleague of 42 Macro CEO Darius Dale. While there may be some erosion in our reserve currency status during the Fourth Turning, we maintain the belief that the United States is unlikely to lose its position as the world’s reserve currency.

Moreover, we could experience a strengthening dollar as lenders and borrowers around the world favor financing in other currencies at the margins, resulting in a continuation of the underlying dollar short squeeze that has been ongoing since 2014. If we do, it would likely necessitate the Federal Reserve to counteract through measures such as currency debasement and financial repression.

Regardless of your outlook on asset markets in the long term, we emphasize the importance of focusing on the current and upcoming Market Regime as the optimal path to navigate through these growing uncertainties.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

What The Pivot to A REFLATION Market Regime Means For Asset Markets

Darius sat down with Julia La Roche last week to discuss the recent transition to REFLATION, inflation, rate cuts, and more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. REFLATION Is Now The Top-Down Market Regime

Last week, we experienced a Market Regime shift from the perspective of our 42 Macro Global Macro Risk Matrix from GOLDILOCKS to REFLATION.

REFLATION introduces a distinct set of Market Regime guidelines that investors should consider for their portfolio construction:

- Risk Assets > Defensive Assets

- High Beta > Low Beta

- Growth > Value

- Cyclicals > Defensives

- Small & Mid Caps > Large Caps

- International > US

- EM > DM

- Spread Products > Treasuries

- Short Rates > Belly > Long Rates

- High Yield > Investment Grade

- Industrial Commodities > Energy Commodities > Agricultural Commodities

- FX > USD

Given that both GOLDILOCKS and REFLATION are both risk-on regimes, investors may not need to make significant adjustments to their portfolios for this particular regime transition.The big pivot investors must make in a GOLDILOCKS-to-REFLATION phase transition is being incrementally longer of Risk Assets relative to Defensive Assets.

2. “Sticky Inflation” Is Likely To Be A Consensus Theme By The End of The REFLATION Market Regime

The January CPI Report revealed signs of sticky inflation:

- Headline CPI accelerated to 2.8% on a 3-month annualized basis, a value above its 2015 to 2024 trend

- Core CPI spiked to 3.9% on a 3-month annualized basis, a value above its 2015 to 2024 trend

- Supercore CPI accelerated to 6.5% on a 3-month annualized basis, a value above its 2015 to 2024 trend

Given the apparent lack of restrictiveness of the current policy in place by the Fed and the resilience of the labor market, a return to 2% inflation seems unlikely at this current juncture.

Moreover, a divergence between CPI and PCE Deflator statistics has emerged in recent months. We believe this divergence is likely to persist for another one to two quarters, allowing the “immaculate disinflation” theme to continue and asset markets to rally during this period.

3. Money Markets Are Pricing In A More Aggressive Rate Cutting Cycle Compared to The Fed’s Dot Plot Projections

The conventional wisdom among average investors is that rate cuts are only observed when the Federal Reserve begins to lower the policy rate. However, the reality is more nuanced – asset markets, not just in the US but across major economies, are deeply influenced by broader financial conditions rather than solely relying on the observed level of the policy rate.

At 42 Macro, we review policy rates set by the Fed, ECB, Bank of England, and Bank of Japan, as well as the overnight index swap rates relative to the policy rate, which reflects market expectations regarding rate hikes or cuts over the next 3, 6, 9, and 12 months. For the past six months, we have consistently observed negative spreads across OIS curves for the Fed, ECB, and Bank of England.

From our standpoint, this suggests that the rate cuts have effectively already occurred. Looking ahead to the next quarter or two, we anticipate observing incremental evidence of eased financial conditions.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!

Will Global Liquidity Push Bitcoin To All-Time Highs?

Darius sat down with Anthony Pompliano last week to discuss the outlook on asset markets, global liquidity, Bitcoin, and more.

If you missed the interview, here are three takeaways from the conversation that have significant implications for your portfolio:

1. While There Is An Elevated Risk of A Short-Term Market Correction, The Outlook For Asset Markets Remains Bullish Over The Medium-Term

The 42 Macro Positioning Model indicated that retail positioning had been heavily overweight stocks.

However, after the recent correction, that overweight positioning has dissipated. Despite this, current positioning data from commodity trading advisors (CTAs) and market-neutral hedge funds suggest the possibility of a further short-term market correction.

Looking ahead, the medium-term perspective is likely to be more optimistic. We are still in GOLDILOCKS, and the 42 Macro Weather Model indicates the Top-Down Market Regime has a high probability of remaining in a risk-on condition, either GOLDILOCKS or REFLATION, over the next three months.

2. Global Liquidity Heavily Influences Asset Markets

The 42 Macro Global Liquidity Proxy, an estimate for Global Liquidity, is calculated by summing the Global Central Bank Balance Sheet, Global Broad Money Supply, and Global Foreign Exchange Reserves ex-Gold.

The 42 Macro Global Liquidity Proxy is highly correlated to most assets, including corporate bonds, treasury bonds, crypto, and stocks. Only trend stationary markets like currencies and commodities fail to have a significantly high degree of correlation and/or correlation to the 42 Macro Global Liquidity Proxy.

Understanding the drivers of global liquidity, such as potential shifts in central bank policies, variations in credit growth across different economies, and other pivotal factors, is crucial for investors. By closely monitoring these drivers and tracking leading indicators of global liquidity, investors can better position themselves to navigate market risks and capitalize on emerging opportunities.

3. Bitcoin Is Likely To Appreciate Significantly Due To Fourth Turning Tailwinds

The flows into the various Bitcoin ETFs over the past couple of weeks suggest growing investor confidence in Bitcoin’s viability. We believe this momentum is likely to continue.

In the context of the Fourth Turning regime, which is likely to span the next decade, our research suggests an environment marked by structurally elevated inflation and budget deficits. These conditions are likely to spark a surge in demand for alternative assets like Bitcoin.

Although there will be periodic downturns, we maintain a long-term outlook that Bitcoin’s value is likely to appreciate significantly.

That’s a wrap!

If you found this blog post helpful:

1. Go to www.42macro.com to unlock actionable, hedge-fund-caliber investment insights.

2. RT this thread and follow @DariusDale42 and @42Macro.

3. Have a great day!