The End of American Exceptionalism?

Darius Dale recently joined Víctor Hugo Rodríguez on Negocios Televisión to discuss why markets may not have bottomed yet—and what needs to change before risk assets become attractive again. If you missed the appearance, here are three key takeaways that likely have huge implications for your portfolio.

1) Markets Won’t Bottom Until Three Things Happen

Darius laid out a clear three-point checklist that must be met before investors can confidently reallocate into risk assets:

- The Fed must expand its balance sheet (i.e., QE or liquidity support).

- Consensus earnings and GDP estimates must be revised lower to reflect recession risks.

- Clarity is needed on fiscal policy—specifically, whether Trump’s tax cut package will actually be stimulative and whether the “DOGE” budget cuts will be softened.

Key Takeaway:

We’re still early in all three of these processes, meaning downside risk remains elevated over the next 2-3 quarters. Investors should expect more volatility until policymakers act decisively.

2) Foreign Demand for U.S. Assets Is Cracking

Darius warned that global capital allocators may be stepping back from U.S. Treasuries and equities. As the U.S. turns away from globalization and fiscal prudence, foreign investors are less willing to finance America’s growing deficits. With Congress potentially adding another $5-plus trillion in debt via tax cuts, this shift could put significant upward pressure on long-term yields.

Key Takeaway:

This marks the potential beginning of a structural regime shift in global capital flows—a bearish signal for bonds and a growing risk to U.S. financial stability.

3) The KISS Model Portfolio Is Positioned for Defense

Months ago, Darius moved his own allocation—and that of thousands of 42 Macro clients—into defensive posture. At the time of recording on Tuesday afternoon, the 42 Macro KISS Model Portfolio featured:

- 67.5% Cash

- 0% Stocks

- 30% Gold

- 2.5% Bitcoin

Key Takeaway:

KISS pivoted to 0% equities on March 5th, and will remain in defensive mode until it quantitatively derived volatility targeting and dynamic position sizing signals inflect. The strategy is designed to minimize drawdowns and preserve capital during cyclical bear markets—while also participating in bull markets.

Final Thought: Wait for the Signal, Not the Noise

Markets are still searching for footing in a rapidly shifting macro landscape. As Darius makes clear, this isn’t a moment for hero trades or blind optimism — it’s a moment for discipline. Until we see a dovish policy pivot, meaningful earnings downgrades, and/or clarity on fiscal direction, staying defensive isn’t just smart — it’s necessary. Risk-on will have its time, but we’re not there yet. Let the checklist, not emotions, guide you.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Tariffs: The Ultimate Stagflationary Shock?

Darius Dale recently joined Jack Farley on The Monetary Matters Network to break down why we remain bearish on U.S. equities, cautious on bonds, and are eyeing a short-term bid in Treasurys. If you missed the interview, here are three key takeaways that likely have huge implications for your portfolio:

1) The U.S. Economy Faces a Slower Growth and Higher Inflation Environment

Darius emphasized that tariffs, policy uncertainty, DOGE, and restricting immigration are creating a stagflationary shock. This is pushing growth expectations lower while raising inflation risks. The Trump administration’s economic restructuring plan aims to shift the economy away from deficit-financed consumer spending toward a more balanced, private sector-driven model—but that transition is likely to be turbulent.

Key Takeaway:

Markets may still be underpricing the magnitude of the economic slowdown. A period of slower growth, rising unemployment, and compressed corporate margins could drive a significant repricing of risk assets from here.

2) A Global Debt Refinancing Crunch Remains the Top Risk of 2025

Darius flagged what he calls a “global debt refinancing air pocket” as the number one risk for investors this year. While debt refinancing needs are surging due to the all-time-low-interest-rate borrowing from 2020 rolling over, global liquidity is not keeping pace. This creates a dangerous imbalance that historically leads to severe dislocations in asset markets. Global debt refinancing risk is being exacerbated by the risks we flagged in callout #1 above.

Key Takeaway:

Unless the Federal Reserve intervenes with QE before a crisis hits, financial instability—especially in credit markets—may force a much sharper correction than consensus expects. The Fed’s delayed reaction function adds to the downside risk.

3) Asset Allocation Must Reflect a Wide Distribution of Probable Economic and Policy Outcomes

Darius highlighted that 2025 presents one of the widest distributions of macroeconomic outcomes he’s seen in his career. With meaningful downside risks in the near term, followed by potential tailwinds (tax cuts, deregulation, QE), investors must be prepared for both a deepening crash and a rapid recovery over the next few quarters.

Key Takeaway:

Sticking with a static portfolio strategy may expose investors to unnecessary drawdowns. Systematic risk-managed approaches, like KISS, that dynamically adjust based on volatility and macro signals could be essential in navigating this highly uncertain environment.

Final Thought: Prepare to Risk Manage a Deep “V”

Markets are entering a treacherous phase—caught between slowing growth, rising inflation, and record levels of debt that need refinancing. With tariffs and fiscal retrenchment amplifying downside risks, the Fed may be forced to choose between maintaining inflation credibility or delivering preemptive liquidity support. Meanwhile, the global capital cycle is turning, and U.S. exceptionalism is starting to fray. Investors must recognize that the range of outcomes in 2025 is unusually wide—and incorporating signals from proven risk management overlays is more critical than ever.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Is President Trump Engineering A Hard Reset?—Darius Dale on Negocios TV

Darius Dale recently sat down with Víctor Hugo Rodríguez to break down the impact of fiscal tightening, global debt refinancing risks, and the Federal Reserve’s next move. If you missed the interview, here are three key takeaways that may have huge implications for your portfolio:

1) The U.S. Economy Is Slowing Faster Than Expected

Darius warns that the U.S. economy is decelerating more quickly than consensus expects, as both fiscal tightening and policy uncertainty weigh on growth. The economy had been artificially boosted by government spending, but that effect is now wearing off. Meanwhile, the federal deficit has surged by 38% this fiscal year and by nearly 30% on a calendar-year basis, increasing the risk of a faster-than-expected slowdown from this artificial sugar high.

Key Takeaway:

Without policy intervention, the risk of a full blown crash in the stock market is rising. The Fed’s response will be crucial in determining whether the market can stabilize. We do not currently anticipate the Fed will be proactive enough.

2) The Global Debt Refinancing Crunch Could Trigger Forced Deleveraging

Roughly 20-25% of global non-financial sector debt must be refinanced in 2025, creating a massive liquidity gap. The key question: Who will absorb this debt? With investor balance sheets stretched and the Fed unlikely to launch QE soon, liquidity shortages could force asset sales and amplify volatility.

Key Takeaway:

Investors should watch credit markets closely—signs of stress here could signal broader market fragility and a sharp repricing of risk assets.

3) Defensive Positioning Is Critical in a Liquidity Vacuum

Darius argues that investor expectations remain too optimistic, despite sizable downside risks to growth. In this environment, capital preservation should take priority. Defensive positioning includes raising cash, rotating up in credit quality, and shifting toward defensive equities like consumer staples and utilities.

Key Takeaway:

The safest sectors in this environment are defensive dividend stocks like utilities and consumer staples, while high-beta cyclical assets tied to trade remain vulnerable.

Final Thought: The Fed’s Dilemma Will Define 2025

The Fed faces a tough choice: stick to its 2% inflation target or intervene with liquidity support to stabilize markets. If inflation reaccelerates while growth slows, the Fed may need to revise its inflation target higher to justify adequate monetary easing. The macro landscape is shifting fast—investors must stay ahead of these critical developments.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Tracking The Invisible Gorilla—Darius Dale & Hugh Hendry on Pro to Pro

Darius Dale, 42 Macro Founder and CEO, sat down with legendary macro investor Hugh Hendry to dissect the Eurodollar system, the Yen carry trade, and the potential for a global liquidity squeeze. If you missed the interview, here are three key takeaways that may have huge implications for your portfolio:

1) The Eurodollar System Fuels the Overvaluation of Everything

Hugh argues that global liquidity isn’t controlled by central banks but rather by the Eurodollar system—an unregulated, highly leveraged financial network that drives global credit expansion. For decades, foreign banks have used U.S. Treasuries, JGBs, and European bonds as collateral to create vast amounts of off-balance-sheet credit, inflating asset prices worldwide. However, as cracks emerge in global markets, liquidity may be tightening faster than investors realize.

Key Takeaway:

The Eurodollar system, not the Fed, dictates market liquidity—watch for signs of stress that could trigger a sharp repricing of risk assets.

2) The Yen Carry Trade Is Unwinding, and It’s Not Over

The Japanese banking system has been a major source of global liquidity, using JGBs to access dollars via Eurodollar swaps. But BOJ tightening amid a U.S. growth scare risks triggering a broader unwind of global risk-taking.

Key Takeaway:

A deepening US growth scare would be a major macro shock, potentially triggering forced deleveraging across global markets.

3) Trump’s Policies Could Engineer a Deep Recession—By Design

Hugh suggests Trump may be embracing a Paul Volcker-style economic shock by deliberately pushing for austerity, tariffs, and aggressive spending cuts. The goal? Trigger short-term pain to force a hard economic reset. Meanwhile, the Fed’s recent rate cuts weren’t about supporting the economy—they were about steepening the yield curve to prevent a flood of mortgage refinancing that could have reignited inflation.

Key Takeaway:

Markets should prepare for policy-driven volatility, as accelerated fiscal tightening collides with delayed monetary easing.

Final Thought: The Death of Money?

We may be witnessing a paradigm shift in global finance. The pillars that have supported market liquidity for decades—the Eurodollar system, Japan’s banking sector, and China’s dollar recycling—are all under pressure. If these liquidity engines unwind, we could see a prolonged bear market and a potential hard reset of the global financial system. The macro landscape is shifting fast—investors must stay ahead of these critical developments.

If you are not confident your portfolio is positioned correctly for the evolving macro landscape, partner with 42 Macro for data-driven insights and proven risk management overlays—KISS and Dr. Mo—to help you stay on the right side of market risk.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Darius Dale on MacroVoices: Investing Amid The Changing World Order

Darius recently sat down with Erik Townsend on MacroVoices for a wide-ranging discussion covering inflation, fiscal dominance, and the impact of the Fourth Turning on financial markets. If you missed the interview, here are three key takeaways that could significantly impact your portfolio:

1) Inflation Is Not Going Back to 2%—And the Fed’s Response Will Be Crucial

Darius argues that inflation is structurally higher in this economic cycle and unlikely to return to the Fed’s 2% target without a full-blown recession. His research shows that inflation is the most lagging economic indicator, typically breaking down only 12-15 months after a recession starts—which is not currently in sight. Instead, inflation is likely to reaccelerate in 2025, driven by tight housing supply, faster credit growth, slowing labor supply, and increased pressure on corporate margins.

Key Takeaway:

The Fed faces a tough decision: stick to its 2% target and risk market turmoil or adjust expectations and let inflation and monetary policy run hotter. The market’s long-term trajectory depends on how policymakers navigate this tension.

2) The Fourth Turning Is Reshaping Fiscal and Monetary Policy

Darius highlights that we are deep into a Fourth Turning, a period of structural great institutional and geopolitical change. Historically, Fourth Turnings bring explosive sovereign debt growth, increased fiscal dominance, and rising inflation, requiring financial repression and monetary debasement to manage oppressive public debt burdens. With deficits spiraling and entitlement spending and net interest growing at a +15% CAGR, fiscal policy is unsustainable and risks a breakdown of the current world order in which the U.S. Treasury sits atop the the global capital structure.

Key Takeaway:

Investors must prepare for an era where monetary easing and inflation become structural tools to manage debt, fundamentally altering portfolio strategies. Holding assets that benefit from financial repression—like equities, gold, and Bitcoin—will be important.

3) Market Regime Shifts Will Drive Investment Success

Rather than making long-term macro predictions, Darius emphasizes trend-following and market regime nowcasting as the best way to stay on the right side of market risk. His 42 Macro Risk Matrix tracks growth, inflation, monetary, and fiscal policy shifts in real-time, helping investors adapt as macro conditions evolve. The biggest risk today? A potential mispricing in bonds and the possibility of term premiums normalizing, pushing yields higher.

Key Takeaway:

Investors need a dynamic framework to manage risk in a fast-changing macro landscape. Relying on old models like 60/40 portfolios won’t cut it—market regime awareness is key to navigating volatility and seizing opportunities.

Final Thought:

The themes discussed—sticky inflation, fiscal dominance, and market regime shifts—all point to a period of profound macroeconomic change. Investors who fail to adapt risk being caught off guard by rising volatility and policy shifts. To stay ahead, it’s essential to incorporate real-time macro tracking and flexible positioning strategies in portfolio management.

Since our bullish pivot in January 2023, the QQQs have surged 82% and Bitcoin is up +293%.

If you have missed part—or all—of this market, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

Thousands of investors around the world use 42 Macro to confidently navigate market shifts and optimize their portfolios. If you’re ready to incorporate macro into your investment process and stay ahead of these monumental changes, we invite you to watch our complimentary 3-part Macro Masterclass.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

The Five-Year Countdown: How AI Will Dramatically Reshape The Economy And Asset Markets

Darius recently sat down with Raoul Pal of Real Vision for an enlightening conversation about the accelerating impact of AI, the exponential age, and what investors must do now to stay ahead. If you missed it, here are the three most important takeaways that could significantly impact your portfolio:

1) The Next Five Years Will Change Everything—Faster Than Expected

Raoul Pal’s “Exponential Age” thesis is happening at an even greater speed than anticipated. With AI advancing at an exponential rate—expected to surpass human intelligence within the next year—the way we work, invest, and interact with markets will fundamentally shift. AI will replace entire job sectors, disrupt business models, and introduce extreme efficiency into capital formation. Investors need to understand that the old rules of economic cycles and the age-old labor vs. capital debate are being rewritten in real-time.

Key Takeaway:

The next five years are crucial—investors who don’t adapt will be left behind. This is the window to build financial security and position portfolios for the seismic shifts ahead.

2) AI and Automation Will Reshape Market Structure

Financial markets will undergo a transformation as AI-powered investment strategies begin to dominate. The firms with the most advanced AI will gain an enormous edge, potentially absorbing vast amounts of market share and capital. At the same time, markets will become both hyper-efficient over the short-to-medium term and hyper-inefficient over the long-term—creating opportunities for those who can navigate the chaos.

Key Takeaway:

The traditional diversification approach (e.g., 60/40 portfolios) will likely underperform. Instead, investors should focus on secular trends such as AI, blockchain, and exponential technologies—these will be the defining investment themes of the coming decade.

3) The Key Risk Is Not Being Over or Under Invested—It’s Being In The Wrong Assets

One of the biggest mistakes investors make is under-allocating to exponential assets. Traditional portfolio management focuses on diversification across asset classes, sectors, and factors, but in this new era, the most successful investors will be those who hyper-concentrate in the right areas. Crypto, AI-focused equities, and cutting-edge technology plays offer the best asymmetric upside.

Key Takeaway:

Investors need to be positioned in exponential assets. Staying on the right side of market risk during the “exponential age” increasingly requires a risk management framework that adapts to rapid change, like our KISS Model Portfolio and Dr. Mo (Discretionary Risk Management Overlay). The size, scope, and rapid pace of change in the economy and asset markets means investors relying on legacy frameworks will struggle—especially as the share of trading activity generated by AI accelerates. Trend following is the best solution to ensure you are participating alongside the supercomputers, not fighting them.

Final Thought: The Time to Act Is Now

If you believe the world will look drastically different in five years, your portfolio should reflect that. The biggest macro opportunity in history is unfolding—don’t get left behind.

Since our bullish pivot in January 2023, the QQQs have surged 86% and Bitcoin is up +316%.

If you have missed part—or all—of this market, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

Thousands of investors around the world use 42 Macro to confidently navigate market shifts and optimize their portfolios. If you’re ready to incorporate macro into your investment process and stay ahead of these monumental changes, we invite you to watch our complimentary 3-part Macro Masterclass.

No catch—just real insights to help you stay ahead in the #Team42 community.

Best of luck out there,

— Team 42

Bitcoin And Stocks Are In For A Wild 2025

Darius recently joined Anthony Pompliano to discuss the outlook for global liquidity, the influence of the U.S. dollar on global liquidity, the potential economic impact of Trump administration immigration policies, and more.

If you missed the interview, here are the three most important takeaways from the conversation that have significant implications for your portfolio:

1. What Is The Outlook For Global Liquidity?

At 42 Macro, we track global liquidity using our Global Liquidity Proxy, which aggregates global central bank balance sheets, global broad money supply, and global FX reserves (excluding gold). We then add a global bond market volatility overlay to simulate the impact of the expansion and contraction of the global repo market.

Our models currently indicate that liquidity is currently moderating—not just globally, but also within most major economies.

We also track the leading indicators of global liquidity, such as stock and crypto market capitalizations, the U.S. dollar and currency volatility, global interest rates and bond market volatility, as well as global growth, inflation, and unemployment.

Our analysis of these leading indicators currently suggests a modest decline in global liquidity over the medium term. Combined with the current downtrend in liquidity across most major economies, this signals an environment that is unfavorable for asset markets from a global liquidity perspective. Rising US liquidity may offset that early in 2025.

2. What Role Will The US Dollar Play In Driving Global Liquidity?

Our research at 42 Macro includes comparing the year-over-year rate of change in our Global Liquidity Proxy to that of the USD Real Effective Exchange Rate and the CVIX. Our analysis indicates there is an inverse correlation between the dollar and global liquidity, as well as between currency volatility and global liquidity.

Currently, the strong U.S. dollar and rising currency volatility are exerting downward pressure on global liquidity. Looking ahead, potential policies under the new administration, such as tariffs and pro-growth, reflationary initiatives, could prompt the Federal Reserve to adopt a less-dovish monetary policy outlook relative to current market pricing, which may further strengthen the dollar.

If these scenarios unfold and we see sustained dollar strength and higher currency volatility, it would create an additional headwind for global liquidity, compounding the pressures already signaled by our leading indicators.

3. How Would Trump Administration Policies On Immigration Likely Impact the Economy?

We have recently highlighted in our research that one positive outcome of open borders and the influx of illegal immigrants has been a significant deceleration in wage growth.

Specifically, the Private Sector Employment Cost Index peaked at around 6% in 2022 and has since slowed to approximately 3%. This decline also drove a sharp deceleration in Unit Labor Cost Inflation, from roughly 6% in late 2021/early 2022 to approximately 1% today.

Reducing the influx of illegal immigrants, even modestly, would likely lead to a tighter labor market, faster wage growth, and higher unit labor cost inflation. Without a corresponding increase in productivity growth, corporate profit growth would likely slow as a result.

Since our bullish pivot in November 2023, the QQQs have surged 42% and Bitcoin is up +176%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it’s time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just high-quality insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.

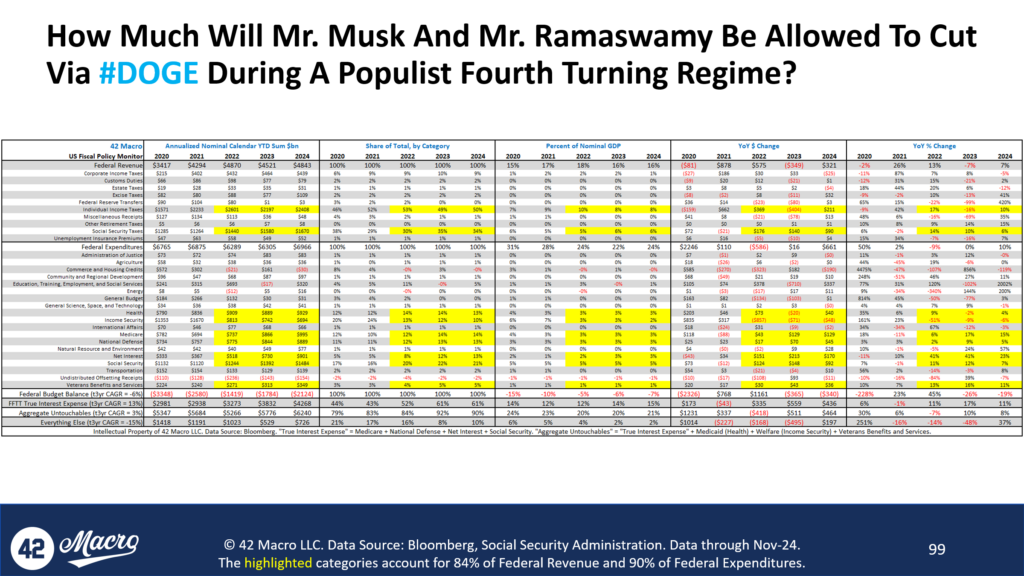

What Must Be Done To Prevent DOGE From Failing?

Darius recently sat down with FFTT Founder and President Luke Gromen to discuss how marketable U.S. treasury market dynamics have shifted over recent years, the likelihood of a meaningful reduction in the federal budget deficit in this Fourth Turning, and more.

If you missed the interview, here are the two most important takeaways from the conversation that have significant implications for your portfolio:

1. How Have Changes In Ownership Structure Contributed To Price And Yield Dynamics In The Treasury Market?

At 42 Macro, one of the ways we analyze the marketable U.S. Treasury market is by segmenting it into various investor cohorts:

- The Federal Reserve: The Fed’s share has been declining due to balance sheet runoff, peaking at 25% in late 2021 and now at only 15% of total marketable Treasury securities.

- Commercial Banks: Banks’ market share decreased from early 2022 until late 2023, when it began to stabilize. This stabilization was driven by programs like the Bank Term Funding Program (BTFP) and expectations that the Federal Reserve would dramatically lower interest rates. Currently, their share is around 15%, well south of the peak of 33% in 2003.

- Foreign Central Banks: The decline in global trade and the steady shift away from global dollar recycling led by the BRICS member nations caused foreign central banks’ share to steadily decline to 14% from a peak of 40% during the 2008 global financial crisis.

- Global Private Non-Bank Sector (Investors): This cohort has become the largest holder of marketable U.S. Treasury securities, with its share increasing from 36% in late 2021 to 55% today.

This shift in ownership has structurally altered the Treasury market. Unlike banks—such as the Fed, foreign central banks, and commercial banks which purchase Treasurys to satisfy policy or regulatory mandates (e.g., Dodd Frank, Basel III and IV)—global investors demand ex ante returns to compensate for taking risk in their portfolios.

As a result of this seismic shift, upward pressure on yields has intensified, signaling a more acute phase in the evolution of Treasury market dynamics and expectations.

2. How Likely Is Significant Reduction In The Federal Budget Deficit During This Fourth Turning?

Our analysis of U.S. federal budget dynamics highlights significant challenges to achieving meaningful deficit reduction.

First, U.S. federal expenditures currently represent roughly a quarter of U.S. GDP—the highest share since at least 1970 excluding COVID and the GFC. Thus, significant cuts would likely catalyze a downturn in the economy—however beneficial a smaller government would be in the long run, which is something both Darius and Luke agree with. Per Luke, the last three recessions saw the U.S. federal budget deficit widen by 600bps, 800bps, and 1,200bps.

Secondly, our research indicates that approximately 90% of the budget is effectively untouchable. This “Aggregated Untouchables” category includes “True Interest Expense”—comprising Medicare, National Defense, Net Interest, and Social Security—along with Medicaid, Welfare, and Veterans’ Benefits. Collectively, these expenditures represent programs unlikely to face cuts under the current pro-populist political climate and are compounding at a rate of +3% per year (+13% per year in the “True Interest Expense” category). The remaining 10% of the budget, which largely includes discretionary spending, amounts to just over $700 billion and has already been shrinking at a compound rate of -15% per year over the past three years.

Lastly, demographic trends are exacerbating the fiscal burden. By 2025, 160,000 people will join the retirement-age population each month, compared to just 32,000 entering the working-age population.

Given these dynamics, meaningful deficit reduction appears improbable without tackling politically protected categories. This leads us to believe that meaningful austerity is an unlikely path forward in the context of this current Fourth Turning environment—especially without a significant devaluation of the US dollar preceding it.

Since our bullish pivot in November 2023, the QQQs have surged 42% and Bitcoin is up +190%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just high-quality insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.

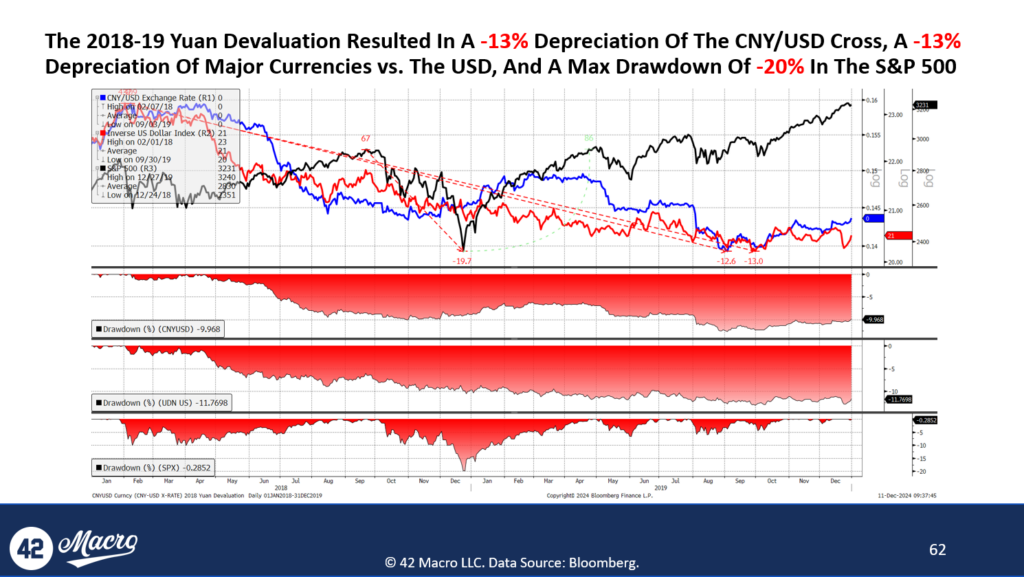

Why Tariffs Are Much Worse For Investors Than You Likely Realize

Darius recently sat down with Bleakley Financial Group CIO Peter Boockvar to discuss the impact of the Trump administration’s proposed tariffs, insights from the 42 Macro Positioning Model, and more.

If you missed the interview, here are the two most important takeaways from the conversation that have significant implications for your portfolio:

1. What Are The Second And Third Order Effects Of Tariffs And How Might They Cause Problems For Asset Markets?

According to data from the Committee for a Responsible Federal Budget, the Trump administration’s proposed tariffs are expected to generate nearly $3 trillion in revenue to help offset the ~$4+ trillion cost of permanently extending the Tax Cuts and Jobs Act (TCJA).

We believe the market is underestimating both the likelihood and scale of these tariffs given that the Congressional budget reconciliation process – specifically the Byrd Rule – will require pay fors to offset the lost revenue from tax cuts. An equally important but often overlooked factor is the potential for retaliation, particularly from China.

Historical examples, such as the Trump-era trade war, illustrate how heightened tariffs can lead to significant devaluations of the Chinese yuan. If this pattern repeats, it is likely to trigger competitive devaluations among other major currencies, resulting in an excessively strong U.S. dollar. In our view, such dollar strength is likely to suppress global capital formation and weigh heavily on U.S. corporate earnings, ultimately creating a significant headwind for asset markets.

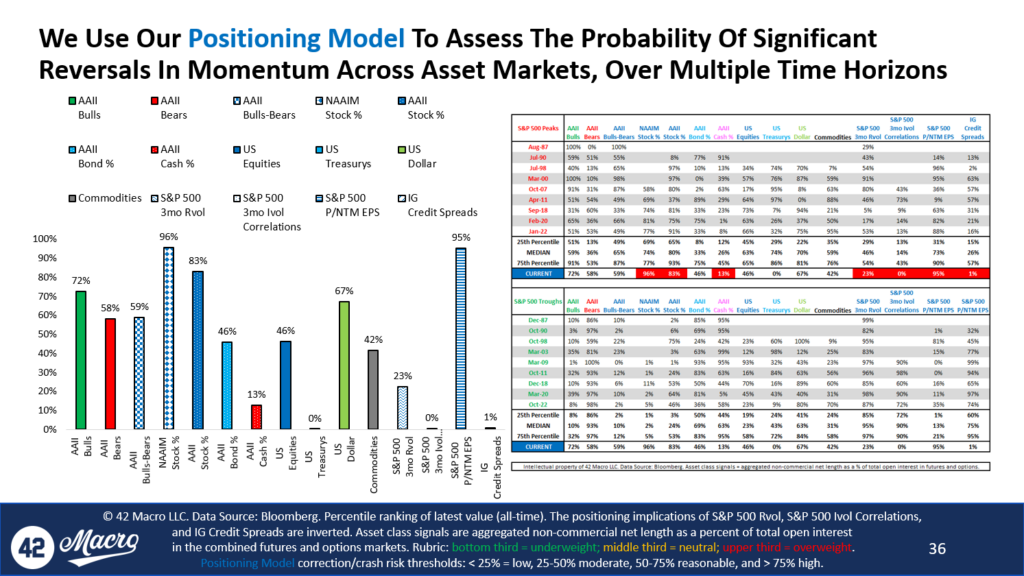

2. What Insights Does The 42 Macro Positioning Model Provide About The Current State of Asset Markets?

Our 42 Macro Positioning Model analyzes a 15 long-term time series, comparing their current levels to the median values observed at major bull market peaks and troughs. Currently, the model indicates several red flags for positioning and sentiment:

- AAII stock allocation exceeds the median value observed at major bull market peaks in the seven market cycles since Jan-98.

- AAII cash allocation is also below the median value observed at major bull market beaks.

- S&P 500 realized volatility—an inverse proxy for systematic fund exposure—is below the median value seen at prior bull market peaks.

- S&P 500 implied volatility correlations—an inverse proxy for market-neutral hedge fund exposure—is below the median value seen at prior bull market peaks.

- S&P 500 price/NTM EPS ratio sits in the 95th percentile of all historical data, dating back to the late 1980s, and is well above the median value observed at major bull market peaks.

- Investment-grade credit spreads are in the first percentile of all historical data, also dating back to the late 1980s, and are well below the median value observed at major bull market peaks.

From a positioning perspective, although these metrics do not necessarily serve as immediate catalysts for reversing the bullish momentum of risk assets, they represent significant potential energy once bearish catalysts emerge. When momentum does reverse, we believe positioning is asymmetric enough to unwind in an aggressive-enough manner to cause a stock market crash.

Since our bullish pivot in November 2023, the QQQs have surged 48% and Bitcoin is up +203%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just high-quality insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.

What Are The Hidden Dangers Looming Over Asset Markets?

Darius recently sat down with Anthony Pompliano to discuss the risks of a stronger US dollar, a potential global refinancing air pocket, and more.

If you missed the interview, here are the two most important takeaways from the conversation that have significant implications for your portfolio:

1. How Can A Stronger US Dollar Cause Problems For Asset Markets?

Our research indicates one significant implication of a strong US dollar is that it pressures foreign investors to repatriate dollar-denominated assets to service the 70% of global debt and 60% of cross-border lending that rely on the US dollar.

The events of 2022 provide a clear example of the potential consequences in such an environment. During a major US dollar rally from January to September of that year, the dollar appreciated by 18%, leading to a reduction in liquidity and severe declines across asset classes, as Gold fell 10%, US equities dropped 25%, US Treasury bonds declined 31%, and Bitcoin plummeted approximately 58%.

Moreover, tariff policies introduced by the Trump Administration, along with potential changes in the Treasury’s net financing policy, may accelerate dollar strength. Coupled with ongoing US economic exceptionalism—driven by tax cuts and deregulation—these factors could push the dollar even higher, increasing the pressure on markets and global financial stability.

If the Federal Reserve’s policy options are constrained by a resilient economy or persistent inflation, it may struggle to prevent the dollar from trending higher, creating significant challenges for asset markets.

2. Is A Global Refinancing Air Pocket On The Horizon?

At 42 Macro, we conducted a deep-dive empirical study on the global refinancing cycle and found it is, in fact, a key leading indicator of global liquidity.

By tracking the year-over-year growth rate of world total non-financial sector debt, lagged by four and a half years to align with typical refinancing timelines, we observe a strong correlation with fluctuations in global liquidity growth. Currently, the lagged growth rate of global non-financial sector debt is accelerating sharply, and our models project this trend to continue through late 2025.

While conventional wisdom suggests this is likely to catalyze an increase in global liquidity, the risk remains that liquidity may fail to expand meaningfully, thus creating a global refinancing air pocket, similar to the divergences observed in 2008-2009, 2011, 2015-2016, 2018-2019, and 2022. If global liquidity fails to follow the path of the year-over-year growth rate of world total non-financial sector debt, we believe it is likely to lead to severe disruptions—or even a meltdown—in global financial markets, negatively impacting asset markets along the way.

Since our bullish pivot in November 2023, the QQQs have surged 44% and Bitcoin is up +184%.

If you have fallen victim to bear porn and missed part—or all—of this rally, it is time to explore how our KISS Model Portfolio or Discretionary Risk Management Overlay aka “Dr. Mo” will keep your portfolio on the right side of market risk going forward.

Thousands of investors around the world confidently make smarter investment decisions using our clear, accurate, and affordable signals—and as a result, they make more money.

If you are ready to learn more about how our clients incorporate macro into their investment process and how you can do the same, we invite you to watch our complimentary 3-part macro masterclass.

No catch, just high-quality insights to help you grow your portfolio—our way of saying thanks for being part of our global #Team42 community of thoughtful investors.