Welcome to The Monthly!

This past month’s market action reinforced just how much uncertainty there remains surrounding the long-term outlook for U.S. monetary policy, even as renewed scrutiny regarding ballooning AI capex budgets drove meaningful dispersion within global equity markets. Cross-asset volatility intensified after the nomination of Kevin Warsh for Fed Chair, while investors simultaneously parsed the deflationary risk AI disruption poses to non-technology industry profits.

The Resilient US Economy continues to recover from its U-shaped slowdown, propelled by fiscal expansion and employment growth in government-adjacent sectors like health care, education, and social services while private-sector hiring remains stagnant. The risk of a jobless recovery remains elevated with meaningful implications for inflation and corporate profits.

In our view, the stock market can still perform well if AI permanently impairs the labor market. Much like globalization and the federal tax code which codifies egregiously preferential treatment to capital income over labor income, AI is simply another tool engineered to consolidate wealth and power. History has already proven that such consolidation is not bearish.

Make no mistake, understanding how these dynamics differ from past cycles is critical for navigating what comes next.

In Case You Missed It

Is Crowded Positioning the Real Driver of AI Volatility?

On Fox Business, Darius joined Maria Bartiromo to discuss why recent volatility surrounding fears of AI disruption are more a function of historically crowded bullish positioning than a deterioration in the structural growth outlook.

Widespread AI adoption is likely to drive a sustained uptrend in productivity, corporate profits, and disinflation, but markets must first work through positioning imbalances.

Could Bank Deregulation Reshape Market Liquidity?

The announcement of Kevin Warsh signals a potential shift in liquidity provisioning from the Federal Reserve back to the commercial banking sector.

We believe that substantial bank deregulation would be required to reduce the Fed’s footprint without destabilizing markets—thus rendering bank deregulation as the only logical choice.

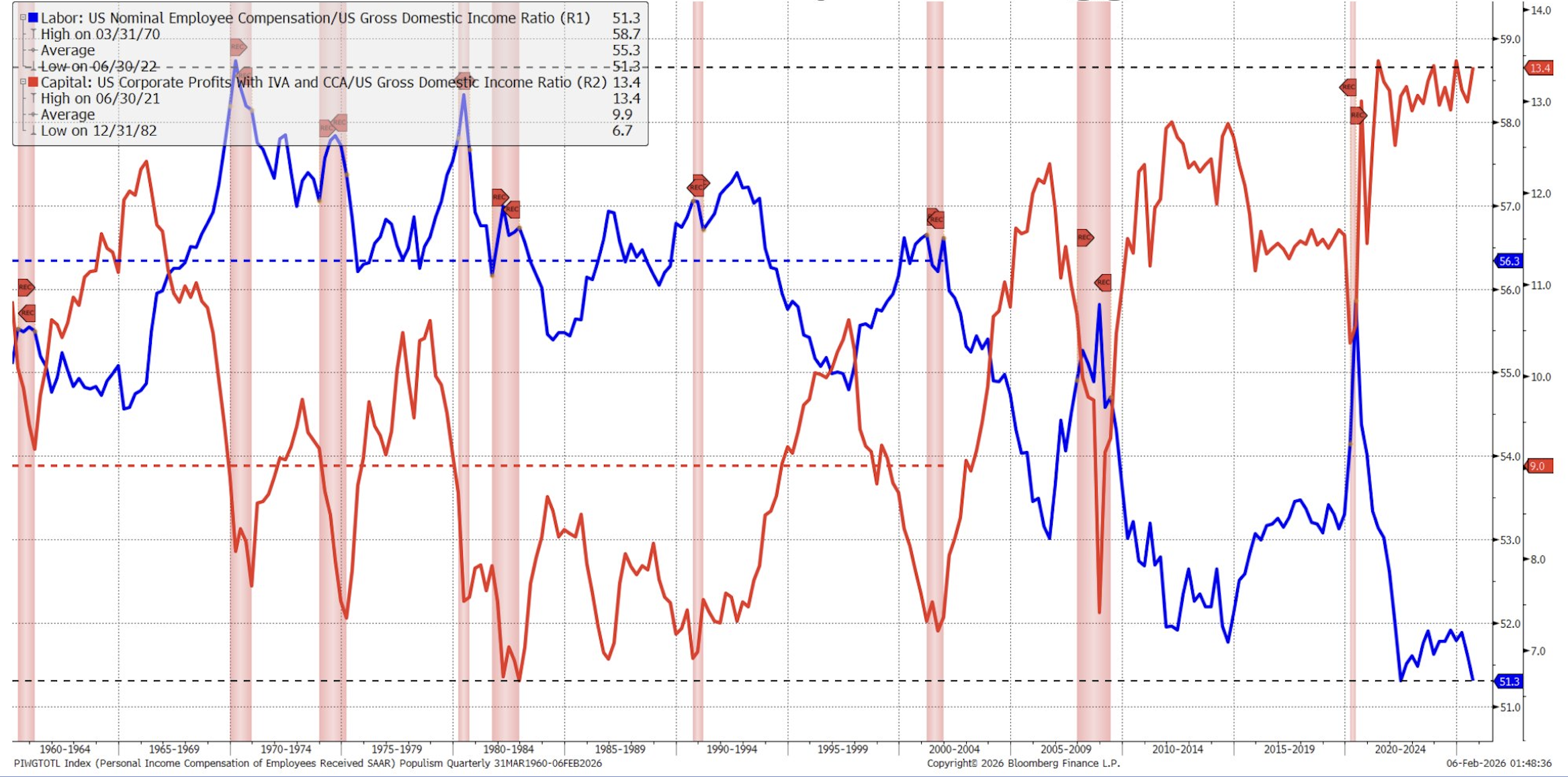

Chart of the Month

The True Promise Of AI Isn’t Mere Efficiency; AI Is An Effective Tool To Cut What Is Still Most Companies’ Biggest Cost — Labor

This chart highlights the long-term tug-of-war between labor’s share of income and capital’s share of income in the U.S. economy. As AI proliferation accelerates, companies are increasingly using technology to compress labor costs, reinforcing a regime of rising margins and productivity gains that supports corporate profitability over the medium term.

Successful Signals From Dr. Mo

On November 29th, 2025, our Discretionary Risk Management Overlay signaled a bullish breakout in Commodity Producers $GNR. Since the pivot, $GNR has appreciated 25%.

Community Spotlight

This month, we’re excited to share feedback from a member of our global investor community regarding the immense value of our risk management signals, which allow them to make high-quality investment decisions in a fraction of the time.

It’s always rewarding to see KISS and Dr. Mo deliver meaningful outcomes for investors around the world. We truly appreciate your feedback.

EXPLORE 42 MACRO RESEARCH