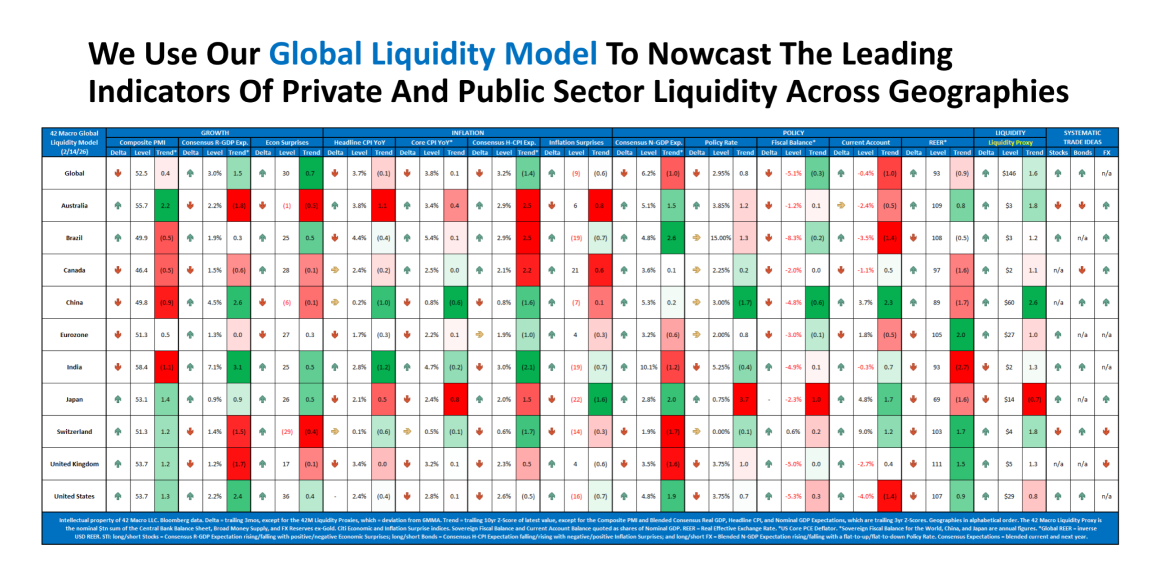

Measuring Liquidity Trends

42 Macro uses the Global Liquidity Model, which is the primary tool we use to nowcast the key cycles that are most predictive of global liquidity trends and forecast their likely influence upon global liquidity and asset markets.

We also use our Global Liquidity Proxy which measures global liquidity by aggregating the U.S. dollar value of major economy central bank balance sheets, broad money supply, and fiat foreign exchange reserves.